Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Reviews

Hasib Anwar

- on December 28, 2021

Blockchain in Payment: Accelerating Payment Services

Blockchain technology is the perfect technology suitable for payment systems. Today, we will take a closer look at the possible benefits of blockchain in payment industries.

Blockchain technology offers faster, low-cost, secured payment services along with a distributed ledger that can provide trust among the participants. Although blockchain started out as the initial support platform for digital currencies, it’s now integrated into various industries, including payments.

In reality, our payment system is full of issues and needs a change right about now. In many cases, it can take days to process a transaction with extra fees and low security. This is the very reason that consumers are shying away from using payment methods to store or transact their money.

Also, a good portion of the population doesn’t even have access to proper banking and payment channels. Blockchain in this regard can really make a change. It can offer them the opportunity they deserve and also reduce all the issues of this sector to a significant extent.

So, in this guide, we will focus on blockchain’s role in the payment systems. Any novice who is curious about the implications of blockchain in the payment industry should use this guide to get more depth about the topic.

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

Blockchain in Payment: Why We Need This Technology?

Many of you may be skeptical about using blockchain or any distributed technology in the payment sectors. However, the industry is full of issues and needs a reality check in the present times. Let’s see what are the major issues or this sector right now!

Please include attribution to 101blockchains.com with this graphic. <a href='https://101blockchains.com/blockchain-infographics/'> <img src='https://101blockchains.com/wp-content/uploads/2020/12/blockchain-payment-methods-.png' alt='blockchain payment methods='0' /> </a>

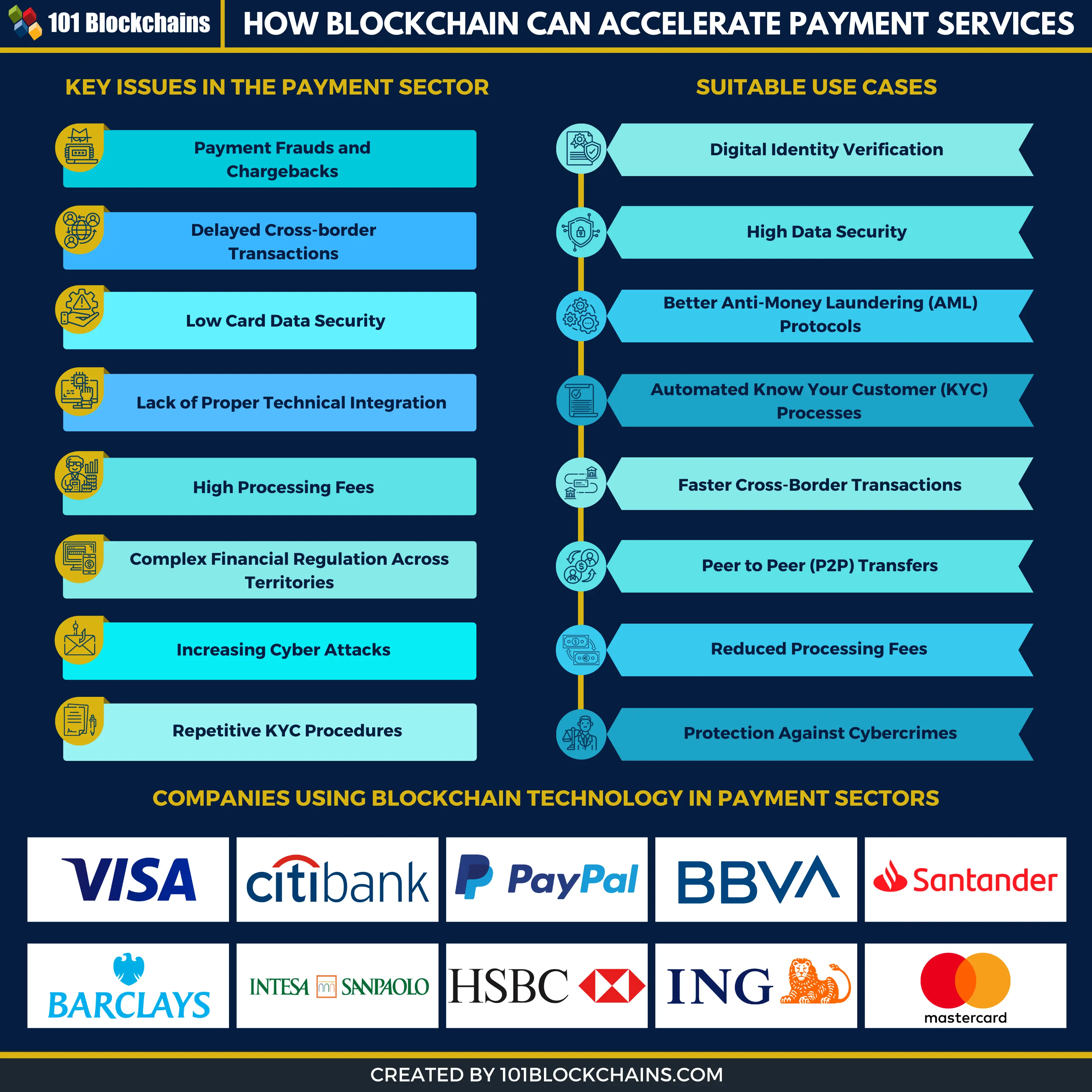

Payment Frauds and Chargebacks

The increasing amount of payment thefts and frauds are quite alarming at the moment. In reality, due to the expansion of the e-commerce sector, the opportunity for misusing the information of consumers or card thefts are happening more aggressively.

Also, chargebacks are really costly, and it can single-handedly damage a business’s reputation. More so, the increasing number of chargebacks can even kill the business as well. The issues are, in many cases, the chargebacks don’t happen for a legitimate reason. So, the fraudulent activities pile up and make it hard for a business to bear in the long run. More so, the theft problems cause massive issues on the customer end, who then lose interest in the brand.

Delayed Cross-border Transactions

It takes a lot of time to process a cross-border payment nowadays. Even if you are not using a banking channel to process the transactions, it can still take up to 6 days to process that. In reality, this can affect the business world quite negatively. Enterprise has to transact money on a daily basis. Also, these transactions have a deadline to meet up. So, any delays in meeting these deadlines would result in massive losses. Therefore, this makes the business process quite inefficient. Also, on a daily basis, many people do send money from abroad to their families. However, when an emergency arises, there is no way for people to send the money immediately. Thus, it causes a lot of misfortunes as well.

Low Card Data Security

A merchant will need a Payment Card Industry Data Security Standards certification in order to accept any debit or credit cards. However, in many cases, merchants fail to comply with all the needs of this certification. In most cases, they tend to ignore the fact that card data security should have the highest priority. That’s why these channels have a very limited amount of security for the customer’s card information. This is something cybercriminals can easily exploit and use whenever they want. Therefore, without a proper security protocol in place, this type of data theft will keep happening.

Difficulty in Currency Conversion

International or global e-commerce needs to accept a variety of currencies and payment methods. More so, electronic payments such as debit/credit cards, mobile payments, or e-wallets need to offer currency conversions efficiently. However, in many cases, these services fail to offer support for certain native currencies, which limits a user’s ability to shop from anywhere.

Again, different payment providers offer different services that come with a lot of fees as well. Overall, the experience can be quite troublesome for both the merchant and the customers. The process of currency conversion isn’t properly streamlining, so that takes time as well. So, the merchant is unable to tap into a lot of potential for more business.

Lack of Proper Technical Integration

Another major issue of this sector is the lack of proper technology integration. What does it mean? Well, it means that even now, payment providers use legacy networks to operate their day-to-day activities. Unfortunately, these legacy networks can’t cope up with the increasing demand of customers and businesses.

Therefore, a lot of errors occur, and transactions or any payment services can take up to days to process. Not to mention the vulnerability of these technologies increase the risk of identity or money theft. However, these organizations are still reluctant to change or integrate new technologies.

High Processing Fees

Well, not every business sees the processing fees as a major issue. However, this is also one of the challenges of this industry. In reality, the processing fees always increase with every year, and in many cases, the variations of processing fees are quite complex. Therefore, it gets quite hard to keep track of the processing fees and how much they would cost in the long run.

Without understanding how these works, you may face issues in your business at an early stage. Also, for the consumers, these are quite unnecessary fees as, in certain cases, it can cost them a lot in the long run, specifically for international transactions.

Start your blockchain journey Now with the Enterprise Blockchains Fundamentals

Complex Financial Regulation Across Territories

Every single country comes with its own set of regulations when it comes to financing or payment processes. However, every time a business expands to new territories, they have to deal with new kind of regulations. This means they have to start or change their business models for every new country. Therefore, the process becomes a lot complex and harder to keep track of.

But without following the guidelines properly, the companies may have to pay fines or even penalties based on the law they broke. This can be a tough situation for small to medium-sized businesses as it can hamper their brand value.

Low Customer Satisfaction

With the rising issues in the payment sector, the customer satisfaction level is dropping at a rapid rate. And why wouldn’t it? The increasing amount of money thefts, identity thefts, and slow services are making the consumers turn away from payment providers. For example, suppose a payment provider stops offering services due to a cyber-attack or discrepancies in their system. In that case, it’s the customer who will have to pay the price.

In this case, the customers who use the cards on a daily basis can’t access the money they have and would face a lot of trouble. It can also take a lot of time to resolve the issue; all of this time, all the consumers will have to look for another option to get their money back.

Increasing Cyber Attacks

The number of cyber-attacks on payment providers is alarming. Well, payment providers are their first target when it comes to cyberattacks. Cyberattacks alone can cost up to $6 trillion every single year in losses. Just imagine the amount of loss that happens from both consumer’s and companies’ ends.

As you already know that the companies don’t offer proper regulations or security protocols in place, it’s quite easy to hack into the system and steal the money or consumer data from it. Therefore, this sector needs a new technology that can help to battle all of the issues without any problems.

Repetitive KYC Procedures

The Know Your Customer or KYC procedures are there for a reason. We know that it’s here to safeguard the payment providers and the consumers from any identity-based issues. However, this process is not as easy as it sounds. In reality, it involves a lot of paperwork and needs a lot of official documentation to verify it.

However, suppose a customer decides to use another payment provider. In that case, he/she has to do the same process all over again. As there is no way for the banks to use the information from other banks to verify it, the consumer has to deal with the same process in a time-consuming way. In the long run, it’s a massive hassle for both the bank and the consumer.

Curious to learn about blockchain implementation and strategy for managing your blockchain projects? Enroll Now in Blockchain Technology – Implementation And Strategy Course!

What Are the Benefits of Using Blockchain in Payment?

Now that you know about the issues of payment industries, it’s time to understand how blockchain can affect it in a positive way. Well, blockchain is still not perfect now, but it can still offer a lot of features for this industry.

First of all, blockchain can offer a more secured platform for transaction processes. In reality, using blockchain for payment processing can open up new opportunities for both the consumer and the company. The cryptographic hash function will ensure that no one can hack into the system and alter its data as they please.

So, blockchain can safeguard the network from both outside and inside attacks.

Again, the blockchain payment platform follows a distributed natured network. So, there is no central governing authority. This can actually be quite positive as the central governing authorities are full of corruption now. So, suppose the central authorities don’t have control over the systems. In that case, consumers can finally trust the system to offer the full security they deserve.

Transparency is another one of the benefits of blockchain in this industry. At present, this industry doesn’t offer any transparency in the system. So, customers don’t know how the companies are processing their money or how they are using it. However, blockchain can give customers their rights back.

Thus, using blockchain-based billing systems can actually pose a lot of benefits for companies and their customer base.

Blockchain comes with a lot of benefits for various industries. Check out our guide on the benefits of blockchain technology to learn more about it.

Use Cases of Blockchain in the Payment Sector

Blockchain in the payment sector can offer a lot of use cases. Let’s check out what these are –

-

Digital Identity Verification

As you already know, identity verification is a lengthy process, and also it doesn’t offer 100% security. That’s why many consumers are skeptical about building or sharing their information for digital verification. Another major point is the time needed for every single verification. In reality, it does take a lot of time to verify every single document.

However, blockchain based payment methods can offer automated processes of identity verification. More so, the overall process of verifying is accelerating compared to the traditional ones. Here, you can upload all your documents, and it will verify them and create a digital identity for you. Obviously, in this case, you will own your digital identity and will have to maintain it yourself.

Curious to know more about digital identity? Checkout detailed guide on Blockchain For Digital Identity

-

High Data Security

Another great use case of blockchain for payment processing is the high security it offers for data. As you already know, merchants fail to comply with all the needs of this certification. In most cases, they tend to ignore the fact that card data security should have the highest priority.

That’s why these channels have a very limited amount of security for the customer’s card information. However, with a blockchain billing system, the scenario can change drastically. In reality, blockchain offers a secured network process where merchants can store the information of the customers, and no one will be able to access it.

This process can actually get rid of any kind of data security problems for good.

-

Better Anti-Money Laundering (AML) Protocols

Due to the lack of Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) protocols, many banks or payment providers fall victim to these illegal activities. For example, HSBC bank had to pay a fine of $1.9 billion in 2012 for getting involved in a money-laundering scheme of the Colombian Norte del Valle cartel and Mexican Sinaloa cartel.

This type of scenario happens a lot, then we can think of. Just because the existing model isn’t capable of handling the situation doesn’t mean this should go on like this. However, blockchain for payment processing schemes can actually alter the scenario for good. Using a blockchain billing system will help honest banks to keep up with the compliances better. More so, they can easily detect any kind of illegal activities that may happen in the long run.

-

Automated Know Your Customer (KYC) Processes

As you already know, the KYC process is not as easy as it sounds. Actually, it involves a lot of paperwork and needs a lot of official documentation to verify it. However, suppose a customer decides to use another payment provider. In that case, he/she has to do the same process all over again. As there is no way for the banks to use the information from other banks to verify it, the consumer has to deal with the same process in a repetitive manner.

But with blockchain based payment methods, a consumer will have to go through the process only once. After that, all of the processes will be automated. In reality, blockchain is a sharable but a secure type of ledger system. So, banks can communicate with each other and use the KYC data from one bank to another. Just think how much time and paperwork it will save!

Get familiar with the terms related to blockchain with Blockchain Basics Flashcards.

-

Faster Cross-Border Transactions

Cross-border payment is an integral part of enterprise businesses. But it takes a lot of time to process a cross-border payment nowadays. Even if you are not using a banking channel to process the transactions, it can still take up to 6 days to process that. In reality, this can affect the business world quite negatively.

On the other hand, blockchain based payment methods can actually offer a faster transaction time. In fact, you can process a transaction within seconds instead of days! Can you imagine the implications of this feature? It can save so many times and would increase the efficiencies of so many businesses.

-

Peer to Peer (P2P) Transfers

Another major use cases of blockchain payment platform are peer-to-peer transfers. In reality, using blockchain technology will help you transact directly with another user. You won’t have to go through a middleman or a central authority to do that.

Although P2P transfer applications are already in the market, they aren’t capable of offering you full freedom as they all come with some form of limitation. For example, they could only support a single geographic location or have a specific zone. But in a blockchain, there is no option for any limitations. You can transact money from anywhere around the globe.

-

Reduced Processing Fees

Processing fees are a big issue when it comes to payment providers. In reality, the burden is for both consumers and businesses as well. In many cases, the processing fees always increase with every year, and in many cases, the variations of processing fees are quite complex. Therefore, it gets quite hard to keep track of the processing fees and how much they would cost in the long run.

But with blockchain based payment platform, there won’t be any need for a middleman. So, you won’t have to pay any processing fees for it as well. This significantly reduces the number of transaction fees for both the businesses and the consumers.

-

Protection Against Cyber-crimes

Another major issue the payment sector deals with is the increasing rate of cyber crimes. This happens due to the companies not offering proper regulations or security protocols when in need. Thus, it becomes quite easy to hack into the system and steal money or consumer data from it.

However, with blockchain-based payment system, you won’t have to worry about cyber attacks ever again. Blockchain is perfectly suited to deal with any kind of cyber-attack. More so, there are even anti-DDoS attack applications based on blockchain that can help you fend off any DDoS attack. Can it get any better than that?

Start learning Blockchain with World’s first Blockchain Skill Paths with quality resources tailored by industry experts Now!

Companies Using Blockchain Technology in Payment Sectors

-

BBVA

BBVA is one of the payments companies that is using blockchain. More so, recently, they completed a syndicated loan with Red Electrica Corporation using this marvelous technology. The best part is that, according to them, the transaction process was so fast that it was a record speed in BBVA’s platform.

-

Intesa Sanpaolo

Intesa Sanpaolo is also another one of the payments companies that are using blockchain technology for their applications. In reality, they are using this technology for validating trading data. Recently, other participants such as Eternity Wall and Deloitte started to test out the technology to see their benefits.

-

Barclays

Barclays is U.K.’s 2nd largest bank at the moment, and they are also in the blockchain ecosystem. At present, they are one of the prominent and active payments companies that are using blockchain for streamlining their KYC protocols and fund transfers. Also, they even have patents against these two features that they implemented in their platform.

-

HSBC

HSBC is also using blockchain in the payments industry. In reality, the bank is already working on a multitude of projects that can facilitate their fund transfers and paperless documentation. So, their investors may track all of their money within the platform.

Also, recently, HSBC Bangladesh competed for the very first cross-border issuance of a letter of credit.

-

Visa

Visa has been working on this technology for some time now. In reality, the company is also using blockchain in the payments industry for dealing with its business-to-business payment services. At present, the project is still alive and thriving.

Without a proper business model in mind, it’s difficult to use blockchain as leverage. Check out our ultimate blockchain implementation strategy to learn more about developing blockchain.

-

Banco Santander

Banco Santander is using blockchain in the payments industry for streamlining their digital identity project. Along with other participants, the company is working on an automated digital identity system. More so, this project can give its user more control over their own data and how they want to use it.

-

MasterCard

MasterCard is one of the payment processing companies that is using blockchain as well. They have a digital currency testing platform that may help the banks deal with CBDC (central bank digital currency) initiative. More so, this platform will demonstrate how the customer can use the currencies to pay in everyday life.

-

PayPal

PayPal is another one of the payment processing companies that is using blockchain to gain more business efficiency. In reality, this company is offering the users to buy, sell, and even hold cryptocurrencies or digital tokens from their PayPal wallets. This will evidently open up new possibilities for the companies in the future.

-

Citibank

Citibank is using a blockchain payment system to modernize the commodity trading processes. In reality, they will use blockchain to offer a better solution for commodity trading financing. This means they will streamline all the financial transactions or contracts in trading through their platform.

-

ING Bank

ING Bank is also using a blockchain payment system in order to test out its privacy technology known as bulletproofs. This will hide the amount in any transactions using bitcoin. This will ensure that all of their client’s information is safe always, and there is no harm done to privacy.

Start learning Blockchain with World’s first Blockchain Career Paths with quality resources tailored by industry experts Now!

Conclusion

In the end, using blockchain in the payment industries can actually help get rid of a lot of the issues without any problems. You can better transaction processing, more security for your data, and ownership of your digital identity. We believe the implementation of blockchain can truly offer benefits for both businesses and customers.

If you are interested in implementing blockchain in your payment systems, then you need to start learning the technology more thoroughly. We recommend starting out with blockchain courses to master the core elements of blockchain before starting your very own project. So, why wait? Take the intuitive right now!