Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Cryptocurrency

Diego Geroni

- on January 15, 2021

What are Retail and Wholesale Central Bank Digital Currencies (CBDCs)?

Central Bank Digital Currencies (CBDCs) have gained prominent recognition in recent times. The following discussion aims to provide a better understanding of the retail and wholesale central bank digital currency options.

Any individual who is aware of the new trends in cryptocurrency and their applications in finance must have heard about CBDCs. Central Bank Digital Currencies have many ambiguities surrounding their classifications and different functionalities.

Although CBDCs have gained prominent recognition, it is highly confusing to find out the extent to which central banks can develop their own digital currency. Additionally, there are many prominent concerns regarding the notable design principles taken into account by central banks in creating their digital currency.

In the following discussion readers can find a detailed impression of a comparative review of both retail and wholesale central bank digital currency. In addition, readers can also explore the underlying motivation for each type of central bank digital currency.

Want to learn about how to build DeFi products interoperably with CBDC? Enroll Now in Central Bank Digital Currency (CBDC) Masterclass

The Road to CBDCs

Before diving into the two notable categories of CBDC, let us reflect briefly on the history of payments. Money is a prominent aspect of economic activity and has been profoundly associated with the needs of users. Therefore, money has constantly evolved into different forms over the course of history with a focus on continuous dematerialization.

In the period of the last few years, internet-based solutions have fostered a radical shift of global transactions towards a digitally connected economy. Many companies capitalized on the opportunity of this shift towards digital commerce and built a formidable reputation as industry leaders. However, we have been able to witness many new innovations recently in the case of payments. The story started with the introduction of Bitcoin, followed by stablecoins based on the Ethereum blockchain.

Transactions worth billions of dollars take place regularly on cryptocurrency platforms, thereby indicating their potential for revolutionizing the payment industry. Cryptocurrency platforms are presenting an appealing value proposition for improving financial inclusion irrespective of the geographical position of users. So, where does a central bank digital currency come into the equation?

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

Perspectives on CBDCs

Central banks are largely focused on maintaining monetary and financial stability. Therefore, the innovations in blockchain and stablecoin technologies have called for central banking institutions to revisit their challenges in event of shifts in the payment industry. One of the most common solutions for central banks, in this case, is the facility of an alternative for private digital payments. This is where the topic of CBDCs comes into the frame, as a digital variant of cash.

Facebook announced its plans for bringing their own digital currency by the name of Libra. Central banks are particularly concerned about the risks for monetary stability and existing fiat state currencies with Facebook’s Libra. Facebook is an online giant with billions of users, and if it introduces its own money, then it can be very stressful for central banks. So, this might be the right time that central banks think seriously about a CBDC alternative.

The successful launch of Facebook Libra presents risks for the monetary sovereignty of central banks. Furthermore, the other roles for Libra apart from the payment function could introduce modifications in standards of the global monetary system. As a result, regulators should also worry about finding potential challenges in managing the monetary system. However, the concept of central bank digital currency was initially frowned upon by central banks.

Basically, central banks were overly cautious about a digital currency issued by a central bank, with varying degrees of cautiousness. While some central banks perceived CBDCs as a ‘wait-and-see’ opportunity, many others disregarded it as a negative factor. On the other hand, the reactions towards central bank digital currencies, especially from central banks and governments all over the world have called for a revised stance on CBDCs. Let us take a look at the factors that drive the potential for developing CBDCs in the present times.

Want to learn the basic and advanced concepts of Stablecoin? Enroll in our Stablecoin Fundamentals Course Now!

-

International Monetary Fund

The International Monetary Fund (IMF) started evaluating the potential for innovation in digital currencies in November 2018. Additionally, it has also shown positive levels of support for proposals to design CBDCs. Top executives of IMF have called central banks to evaluate the functionalities of CBDCs for addressing public policy goals. IMF has pointed out the benefits of CBDC for improving privacy in payments, financial inclusion and consumer security.

-

Bank of International Settlements

The Bank of International Settlements (BIS) has also turned its stance on digital currencies issued by central banks. Executives at BIS feel strongly that big tech giants could dominate the monetary ecosystem with ease by leveraging network effects. Presently, BIS is supporting the efforts of various central banks for research and development of digital currencies on the basis of national fiat currencies.

BIS primarily perceives central bank digital currencies as an instrument for new comprehensive public policy to tackle the entry of big tech giants into financial services. On the other hand, BIS has also expressed uncertainty over the potential implications of introducing CBDCs on stability of global financial system.

-

The People’s Bank of China

The People’s Bank of China is also ramping up its efforts for bringing in a new government-supported digital currency. Also, the People’s Bank of China is the central bank of China, and its new digital currency also focuses on achieving a remarkable position in the worldwide cryptocurrency competition.

Presently, the central bank is leveraging market-oriented institutions for joint research and development of central bank digital currencies. Furthermore, the new central bank digital currency can serve as a new monetary policy tool or investment asset. On the other hand, the central bank digital currency could also serve as a benchmark for interest rates offered by banks on deposits.

China is launching DCEP project that is backed up by the government and is meant to become the new national currency. Learn more about the DCEP project now!

-

European Central Bank

The European Central Bank has also taken a positive stance on the topic of central bank digital currencies. The ECB has drawn attention towards classification of CBDCs according to their purpose. It has specifically focused on verifying whether CBDCs should be in the retail or wholesale category.

The executives at the ECB have stated that retail CBDCs could serve useful for the general public. On the other hand, wholesale CBDCs are likely to suit the objectives of financial institutions. So, this is where we encounter the concept of retail and wholesale CBDCs for the first time! Now, you must be excited to explore more details about these two categories of CBDCs.

The information presented till now offers a clear impression of the necessity of CBDCs as perceived by global financial institutions. However, it is also important to reflect on the critical factors that drive the development of CBDCs. Let us take a look at the reasons to opt for CBDCs in the present times as follows.

Start your blockchain journey Now with the Enterprise Blockchains Fundamentals

Why the Drive for CBDCs?

It is clear that central banks are gradually taking a favorable stance towards introducing their own CBDC. Here are some of the notable arguments that call for introduction of central bank-issued digital currency.

Central bank digital currency is a reliable option for transformation towards a cashless society. They can prompt the replacement of physical payments with electronic payments. Furthermore, CBDCs can also serve as payment instruments with better levels of security and liquidity. CBDCs also enjoy the potential for reducing cash management costs because all transactions are easily traceable and are digital variants.

The shift of central bank money to digital currency can also introduce a shift from an informal-based economy to formal-based economy. As a result, the economy could focus more on efficiency, tax-orientation and transparency. At the same time, the shift towards blockchain based central bank digital currencies can improve the impact of monetary policy.

Increasing Benefits Of CBDC

CBDCs can restrict the scope of substituting cash that can help in avoiding negative interest rates. Implementation of CBDCs can enable the use of new monetary policy tools. On the other hand, CBDCs can also help in increasing aggregate demand that can resolve the demands of monetary policy of central banks focused on price stability.

Many of the proposals for CBDCs, particularly in emerging economies, focus on financial inclusion. With a majority of population facing a lack of banking services or access to commercial banks, CBDCs can foster digital economies. As a result, they can serve as credible tools for improving social and economic inclusion.

The regulatory framework associated with CBDC can also provide lower entry barriers for new entrants in payment industry. In addition, new entrants can also offer payment accounts to customers and increase the level of competition for existing banks. As a result, many non-banking institutions and smaller banks can avoid depending on larger banks for running their payments.

Finally, the most important argument in favor of central bank digital currencies draws attention to a financial system with better efficiency and safety. CBDCs can bring enhancements in existing wholesale financial systems. For example, CBDCs can simplify cross-border payments and settlement systems, interbank payments and settlement systems and delivery versus payment systems.

Individuals, non-banking financial institutions and private sector companies can settle directly with central bank money without any cash deposits. As a result, they can face lower risks of liquidity concentration and credit risk across payment systems. Subsequently, large banks are likely to lose their systemic importance slowly. Therefore, CBDCs are ideally suitable alternatives to bank deposits with considerably lower risks.

U.S. is developing a new kind CBDC project, which is called digital dollar. Here’s a comprehensive guide on digital dollar project and digital dollar wallet.

Categories of CBDCs

Based on the multiple favorable factors for central bank digital currencies, it is clear that they can spell new changes in the global monetary and economic system. However, CBDCs are classified into two different proposals depending on the target user base. The two most common types of CBDC proposals that you can encounter are as follows,

- Retail central bank digital currency

- Wholesale central bank digital currency

On the other hand, readers should also note that there are many CBDCs with the traits of retail and wholesale. So, let us take a deeper look into both types of CBDCs for addressing the actual agenda of this discussion.

-

Retail CBDCs

Retail central bank digital currency focuses specifically on the general public. Generally, the retail CBDCs based on distributed ledger technology include the features of availability, anonymity and traceability. At the same time, they can also offer the possibilities for an interest rate application. The retail CBDCs are particularly renowned among central banks located in emerging economies.

The primary reason for the popularity of retail CBDC is the motivation for capitalizing on opportunities for growth in fintech. Additionally, it promotes financial inclusion alongside presenting a faster shift to a cashless society. Furthermore, retail CBDCs also helps in reducing the costs of cash printing and management.

Key Factors

Now, let us take a look at the key factors that are the underlying principles for retail CBDCs as follows.

- Retail CBDCs are most suitable for the liability side on the balance sheet of the central bank.

- Upon launching, retail CBDCs can present a new variant of central bank money. Subsequently, CBDC is also subject to the central bank functions of issuing, management and controlling. Subsequently, the supply of retail CBDCs will also focus on the country’s monetary policy.

- Distribution of CBDCs is associated with one-to-one parity at par with the relevant fiat currency by the central bank. At the same time, the CBDCs should have support for seamless and flexible conversion against cash and commercial bank money.

- Banks or businesses could develop retail CBDCs on open infrastructures for allowing other businesses for creation of services and products over it.

- Another critical highlight of retail CBDCs is the fact that users don’t need a bank account for accessing or obtaining the digital currency. Additionally, the transaction cost associated with retail CBDCs should be lower than current charges.

- Most important of all, retail central bank digital currencies must be accepted as a legal tender and a mode of payment. The CBDCs should also serve as a safe store of value for citizens as well as government agencies and enterprises.

-

Wholesale CBDCs

The next notable category of CBDCs directly refers to wholesale CBDCs. The wholesale CBDCs are suitable for financial institutions holding reserve deposits in a central bank. The wholesale central bank digital currency can help in improving efficiency of payments and security settlement. Additionally, it also resolves the concerns of liquidity and counterparty credit.

Value-oriented wholesale CBDCs can ensure replacement or support for reserves in the central bank through a restricted-access digital token. The token would serve as a bearer asset in wholesale central bank digital currencies. As a result, the sender will transfer value to the receiver during the transaction without any intermediaries.

Therefore, the new system would differ considerably from the existing system. The existing system involves central banks crediting and debiting the accounts of customers without transfer of the actual values. Wholesale CBDCs are considered as the most favourable alternative for central banks. They have exceptional capabilities for improving the speed and security of wholesale financial systems while reducing costs.

According to the BIS, wholesale CBDC can present potential benefits for payment and settlement systems. The performance of wholesale CBDCs in different experiments conducted and examined already by central banks also presents their potential advantages. The CADcoin in Canada under the Project Jasper and Project Ubin in Singapore, as well as Project Stella in the Japan-Euro Area, are some of the top examples of wholesale CBDCs.

Watch on-demand virtual conference on digital assets and Central Bank Digital Currencies (CBDCs) now!

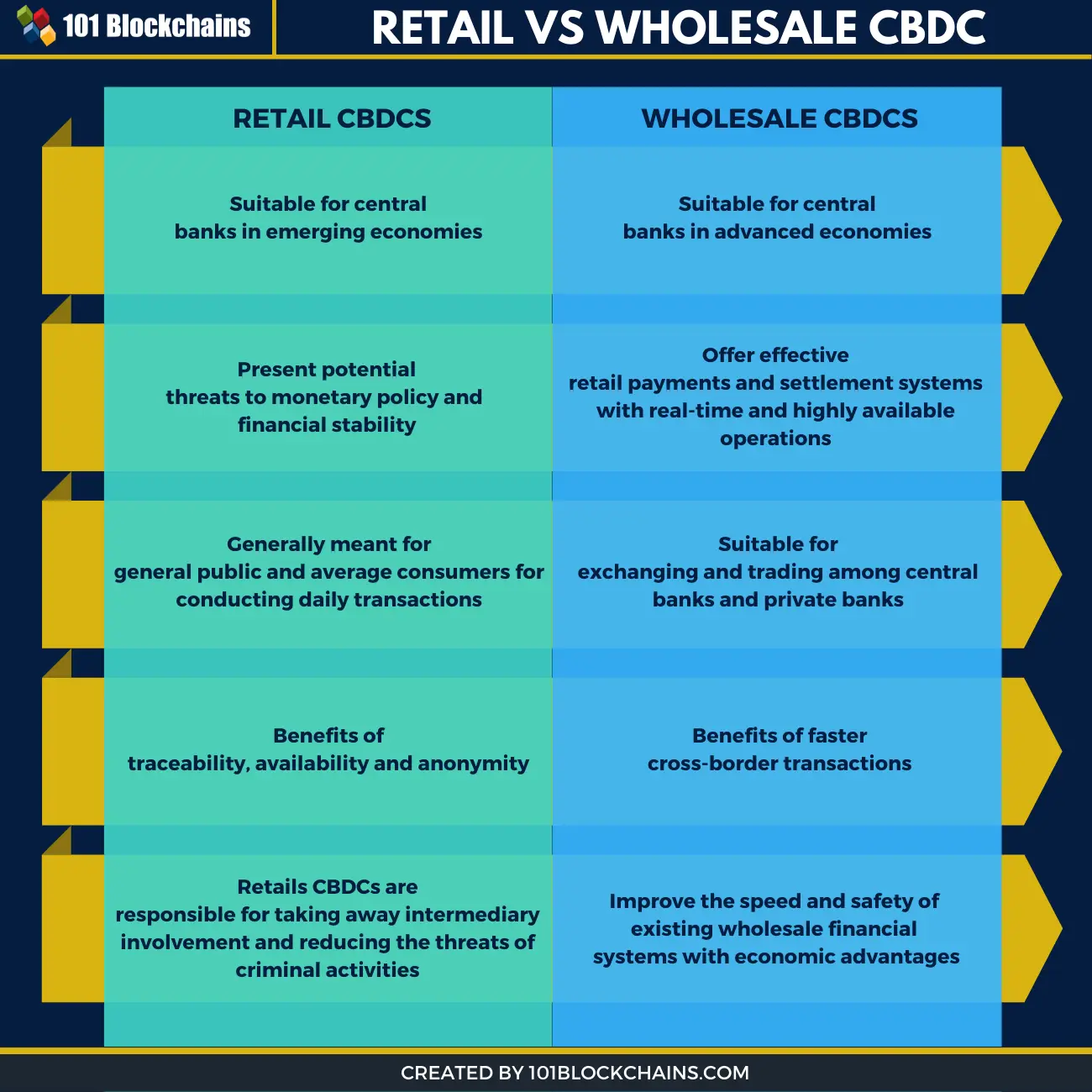

Retail Vs Wholesale Central Bank Digital Currency

So, how do the two central bank digital currencies perform against each other? In comparison to advanced economies, central banks in emerging economies are more eager about retail CBDCs. This factor is not surprising anymore, as many central banks don’t want to create conflict between central bank currency and private sector money. It is also important to consider the restrictions on potential advantages of utilizing retail CBDC.

In the case of advanced economies, retail CBDCs can be an overstatement. When a central bank issues a digital currency that allows almost everyone to store value and make payments through electronic central bank money, financial stability and monetary policy face various risks. Therefore, retail CBDCs presents a notable limitation in this regard. On the other hand, wholesale CBDCs can introduce a series of advantages.

Apart from the efficiency of retail payment and settlement systems with wholesale CBDCs, users can monitor them in real-time with better availability. Presently, majority of citizens enjoy financial inclusion with the widespread use of cash across most of the European countries. The advantages of wholesale CBDC also allow support for linking with other platforms. Wholesale CBDCs allow users to link securities or forex platforms directly with cash platforms.

As a result, they can improve speed of transactions while eliminating the risks of settlement. Furthermore, instant wholesale central bank digital currency systems can improve the speed of settlement on OTC markets and syndicated trade finance and lending. Wholesale CBDCs also foster simpler cross-border payment systems by effectively reducing the number of intermediaries.

You can reflect on a summary of the differences between retail and wholesale CBDCs in the following table.

Please include attribution to 101blockchains.com with this graphic. <a href='https://101blockchains.com/blockchain-infographics/'> <img src='https://101blockchains.com/wp-content/uploads/2021/01/central-bank-digital-currency.png' alt='central bank digital currency cbdc='0' /> </a>

Conclusion

As you can notice clearly, central bank digital currencies might be the next big thing in the world of money. The growing popularity of CBDCs would largely rely on the advantages associated with wholesale CBDCs. They are capable of ensuring limited disruption while ensuring cost-effective global payments.

At the same time, users can also get the advantages of security and speed for their transactions with wholesale CBDCs. So, what is the next step for central bank digital currency? This is where central banks can exert their dominance over the general financial ecosystem all over the world.

On the other hand, central banks are facing a shortage of expertise for developing CBDCs. Start exploring more about central bank digital currency features, use cases and implications with our Central Bank Digital Currency (CBDC) masterclass. Aspiring to become an active part of the development of CBDC ecosystem? Start with our Certified Enterprise Blockchain Professional (CEBP) course and become a certified expert!

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!