Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Cryptocurrency

Diego Geroni

- on September 16, 2021

Understanding the Types of Central Bank Digital Currencies (CBDC)

Want to know about the different types of Central Bank Digital Currencies (CBDC)? Go through this detailed guide on the types of CBDCs to understand them better.

The formidable revolutionary transformations in the world of financial services over the years have completely changed conventional perceptions. The impact of digital transformation on financial services was not limited only to a change in the platform for services. On the contrary, many technological advancements over the years have transformed our traditional views on financial services.

Now, blockchain has enabled flexible access to highly secure, transparent, and faster financial services. Following this trend, many central banks are also evaluating CBDC types to find out possibilities for issuing their own digital currencies in the future. The interest in central bank digital currencies has been increasing due to a wide range of factors. Let us find out how different types of CBDCs have unique characteristics and discover more about their potential.

Excited to build DeFi products interoperably with CBDC? Enroll Now in Central Bank Digital Currency (CBDC) Masterclass

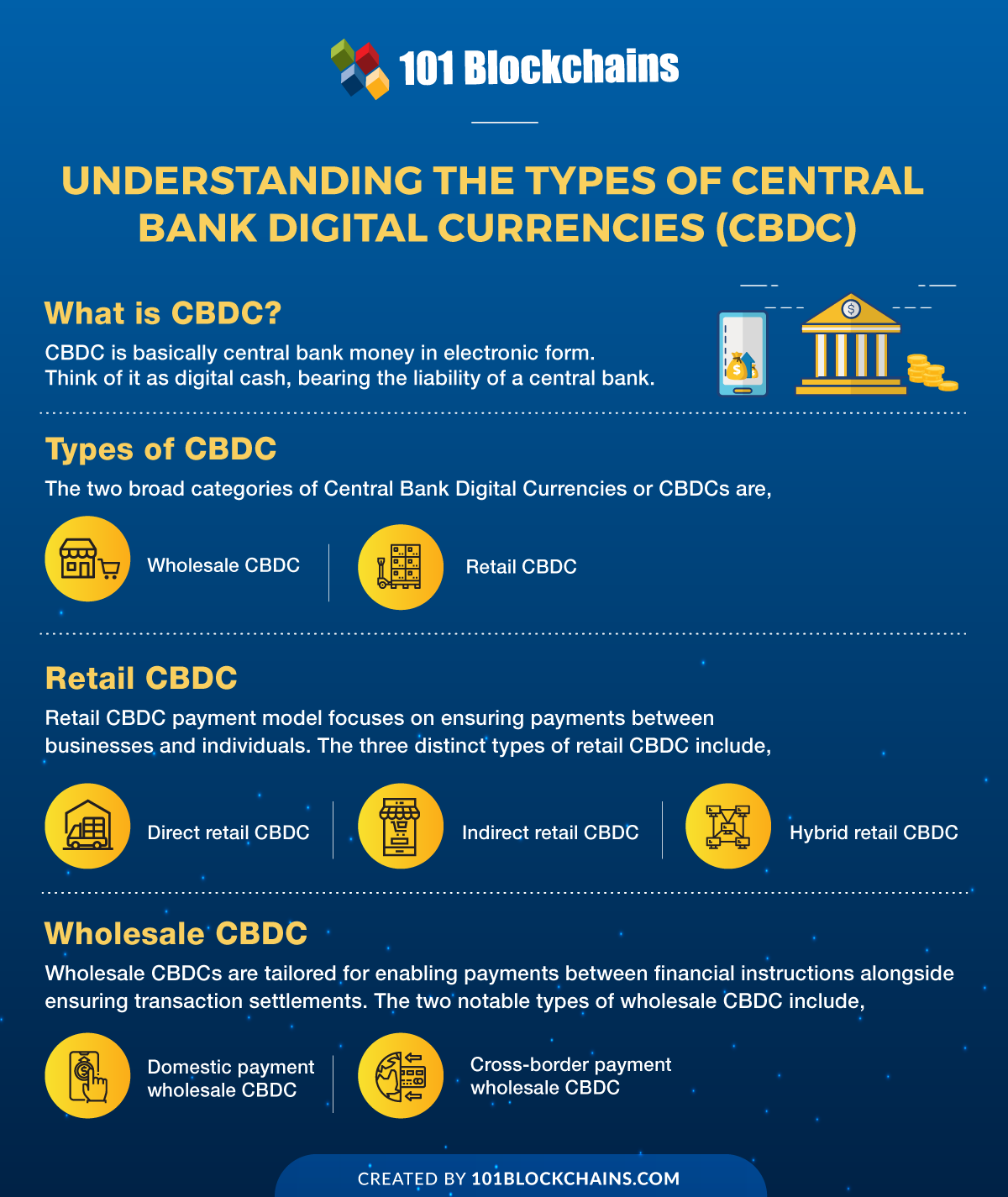

Brief Overview of CBDCs

One of the foremost difficulties in understanding CBDCs (Central Bank Digital Currencies) Types is the lack of a clear definition. CBDCs do not have any particular definition and could point towards different directions based on the perception of the audience. The most general explanation for central bank digital currencies is that they are a new variant of central bank money.

So, you can think of them as a digital currency with central bank liability, featuring denomination in an existing unit of account. Digital currency could serve as a store of value as well as a medium of exchange. The Bank of England provides a more streamlined definition of CBDCs, referring to them as electronic central bank money. In addition, the Bank of England also states some important traits for CBDCs such as,

- CBDCs are more broadly accessible in comparison to reserves.

- CBDCs offers improved support for retail transactions in comparison to cash.

- CBDCs must run on a distinct operational structure in comparison to different forms of Central Bank money.

- CBDCs could also be interest-bearing in case of realistic assumptions of paying an interest rate that is different from the reserve rates.

Another interesting aspect in the definition of CBDCs, related to the CBDC architecture, shows the possibilities for different categories. It is clear that CBDC is an electronic form of central bank money. At the same time, it is also important to note that CBDCs can be held by financial institutions as well as the public. Depending on these two tenets, you can find two distinct models which establish the classification of CBDCs.

Want to learn about Blockchain Solutions for CBDCs? Read here for a detailed guide on Blockchain Solutions For Central Bank Digital Currency (CBDC) now!

Different Categories of CBDCs

The discussion on types of CBDC would ultimately round upon two distinct models of central bank digital currencies. The first model is referred to as retail CBDC, and the second model is known as wholesale CBDC. Let us reflect on these two models to understand Central Bank Digital Currencies Types in detail.

Retail CBDC Model

The retail CBDC model generally focuses on ensuring payment between businesses and individuals. Such a type of CBDC architecture clearly shows low value, albeit with a larger volume. In addition, the retail CBDC model follows the use of various payment instruments flexibly.

Even if cash is a common method of payment, various retail payments still find feasible ways for execution through cards as well as online transfers. The organization of the electronic retail payment systems worldwide features a lot of similarities. The general arrangement of electronic retail payment systems includes three different processes such as clearing process, settlement process, and transaction process.

- The transaction process involves the dispatching and delivery of payment instructions. The transaction process also focuses on verification and authentication of the transaction originator and beneficiary. In addition, it also focuses on validation of payment instructions.

- The clearing process emphasizes matching and processing the payment data. Furthermore, the most crucial function in retail electronic payment for the clearing process points to the calculation of settlement claims and obligations. In addition, the clearing process also ensures the suitable transmission of payment data to the settlement agent.

- The settlement process is the final addition in the retail payment model, which takes care of fund transfer among relevant parties followed by required verifications. After the settlement process, all the relevant parties receive a confirmation of credit or debit.

All of these lead to prominent issues which call for the introduction of retail CBDC types. Retail CBDCs can be available to the general public through two distinct forms, such as digitally issued tokens and deposit accounts in a central bank. For deposit accounts, businesses and individuals could open accounts at their related central bank alongside reaping the advantages of similar services from commercial banks.

By leveraging the deposit accounts, users could initiate and receive transactions alongside viewing their account balance. The other types of CBDC in the retail model include digitally issued CBDC tokens. The digitally issued tokens provide representation for an electronic alternative to coins and banknotes. Only a central bank has the power to issue these tokens to commercial banks for distribution.

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

Types of Retail CBDC

The key highlight of both CBDC types in the retail model points to the difference in verification required for usage. CBDC tokens must go through authenticity verification, such as spending history details. CBDC deposit accounts would require verification of the account holder, such as KYC procedures. Let us take a look at some of the notable variations of retail CBDC.

- Indirect Retail CBDC

The indirect retail CBDC is one of the common Central Bank Digital Currencies Types with considerable similarities to existing retail payment processes. You would need an intermediary layer of financial institutions for setting up an indirect retail CBDC. Such intermediaries take care of onboarding and communications with businesses and individuals, as well as sending payment messages to financial institutions.

- Direct Retail CBDC

The direct retail CBDC solutions focus on businesses and individuals holding ownership of CBDCs by leveraging central bank private accounts. Therefore, intermediaries are not necessary for the direct retail CBDC types. The central bank is responsible for the onboarding and management of financial services. However, new developments in the direct retail CBDC model would encourage the involvement of intermediaries among users and central banks.

- Hybrid Retail CBDC

The hybrid retail CBDC offers a blend of indirect and direct retail CBDC variants. You can find an intermediary layer of financial institutions in hybrid retail CBDC. However, individuals and enterprises could enjoy a direct claim of a CBDC at the concerned central bank. One of the significant implications in this scenario is that intermediaries can maintain the separation of CBDC from the balance sheets. As a result, the enterprises and individuals could have more profitability.

Want to learn about the design and architecture of retail CBDC? Check here Central Bank Digital Currency: Know The Architecture Of Retail CBDC now!

Wholesale CBDC Model

The second broader classification of CBDC architecture takes us to the wholesale CBDC model. The wholesale CBDC model could facilitate payments alongside settlement of transactions among financial institutions. Now, it is important to note that banks already enjoy the facility of directly accessing electronic central bank money.

On the other hand, wholesale CBDC types could offer improvements in risk management and efficiency of the settlement process. In addition, wholesale CBDC is also applicable for asset transfers dealing with securities. You can discover two wholesale CBDC types according to their implementations.

- Domestic Payment Wholesale CBDCs

The majority of wholesale transactions in the present times are associated with a large value, shorter settlement times, and institutional participants. Wholesale transactions and systemically important and could be routed generally through central banks working on real-time gross settlement (RTGS) systems responsible for the execution of these payments.

The example of two large-value payment systems in Europe, such as EURO1 and TARGET2, showcases the use of wholesale types of CBDC. TARGET2 is under the ownership and operational control of the Eurosystem. Domestic payments in TARGET2 generally begin with the originating bank issuing instructions for paying the beneficiary’s bank.

The system would then complete reconciliation, confirmation, and finally completion of the transaction by ensuring fund transfer between bank accounts. The domestic wholesale CBDC would function in the same way with particular emphasis on areas that need faster, reliable, and high-value domestic payments with security.

- Cross-border Payment Wholesale CBDCs

The use case for implementation of wholesale CBDCs for cross-border payments is important than domestic wholesale CBDCs. Presently, cross-border transactions rely on various intermediaries alongside jurisdictions pertaining to single payments. In order to solve the problems of cross-border transactions, wholesale CBDCs can be crafted in three different scenarios. You can have local wholesale CBDCs, local transferable wholesale CBDCs, and universal wholesale CBDC.

Apart from the classification of wholesale CBDC types for domestic and cross-border payments, you could also find wholesale CBDCs for secure transactions. Such types of CBDCs could play a huge role in supporting the tokenization and digital transformation of the security value chain.

Become a memeber now to watch on-demand virtual conference on Digital Assets and Central Bank Digital Currencies (CBDCs)!

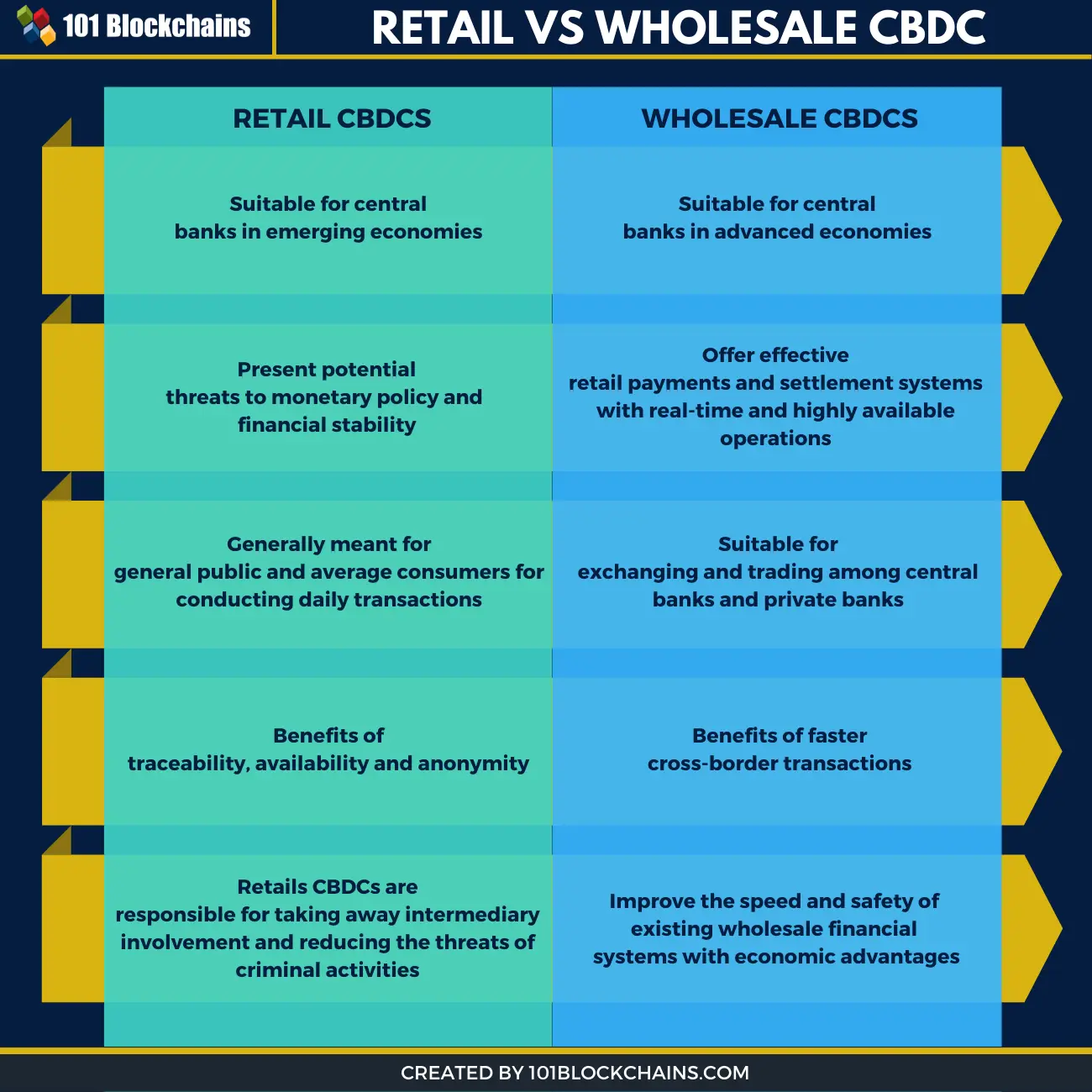

So, we discussed the different types of Central Bank Digital Currencies (CBDC) in above discussion. Below infographics will help you know the difference between Retail and Wholesale CBDC –

Final Words

The most important aspect to note in the case of different types of CBDC refers to their value advantage. CBDCs can open avenues for simpler, faster, and efficient transactions irrespective of geography. In addition, CBDCs bring the inherent benefit of various traits of blockchain technology. The study of different variants of CBDCs clearly shows how one simple concept could be implemented through different models.

The retail and wholesale CBDC models feature distinct scenarios which offer the possibility for further classification of CBDCs. In the long run, the efficiency of the retail and wholesale CBDC types for different use cases establishes their credibility. Learn more about CBDCs to understand them better.