Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Cryptocurrency

Gwyneth Iredale

- on July 05, 2021

Advantages of Central Bank Digital Currencies (CBDCs)

With so much hype about CBDC all around, are you wondering about the advantages of central bank digital currency? If yes, you have reached the right place.

The banking and financial services domain has recently been through considerable levels of digital transformation. New processes such as e-trading, e-KYC, mobility experiences, and digital services are gradually gaining attention all over the world. Basically, the way we deal with money has evolved over the course of centuries through the adoption of new services.

Central bank digital currency (CBDC) is one of the most common topics of discussion nowadays among central banks all over the world. The advantages of central bank digital currency are essential examples of the use of innovative technologies for creating a new form of money.

Although CBDC has the necessary attributes for transforming the financial industry, it is reasonable to wonder about its advantages. Certain financial institutions have already started exploring the possibilities of issuing CBDC as a common accessible variant of money. With the backing of central banks, CBDCs can offer many crucial value advantages over the existing digital currency variants. The following discussion offers detailed insights into the advantages of CBDC for understanding its significance.

Learn how digital currencies can improve your access to financial services, Enroll Now in Central Bank Digital Currency (CBDC) Masterclass

Understanding the Fundamentals of CBDC

One of the first things that you should do for understanding the benefits of central bank digital currency is to learn the fundamentals and background of CBDC. The definition of CBDC and why it was needed in the first place could help you obtain a clear impression of its benefits.

Changing Faces of Money

For many years, money has been an integral part of the economic landscape of civilizations all over the world. We have witnessed money go through multiple phases such as bartering, coins, and then paper-based money. Recently, we have also witnessed the impact of digitalization on introducing e-money. So, what role does money serve in general? The three specific aspects which money clearly indicates are,

- Medium of exchange for purchasing and selling products or services

- Store of value for working as an asset capable of sustaining value of a given period of time

- Unit of account for pricing of a specific product or service alongside the denomination of a specific debt

A major portion of the money you see today, in the form of coins, paper-based bills, and electronic equivalents, is referred to as fiat currency. Central bank money primarily includes cash, mainly including a digital form of reserves housed at the Federal Reserve Banks. The reserves are useful for banks in clearing and settling any obligations among each other. The reserves are also helpful for the Federal Reserve as an instrument for implementing monetary policy.

On the other hand, it is also important to understand the definition of commercial bank money or private money. It is also available in digital form as deposits across insured depository institutions. As a result, debit card transactions at the point of sale, electronic payroll deposits, and Zelle or Venmo payments could present reliable examples of transferring commercial bank money.

Watch on-demand virtual conference on Digital Assets and Central Bank Digital Currencies (CBDCs) now!

The Origins of CBDC

The adoption of different forms of money led to the focus on the advantages of CBDC. Specialized payment providers offering e-money are capable of responding to people’s demands and the economy’s needs. As a result, they can address the requirements of convenience and wider financial inclusion. On the contrary, money issued by private providers does not bear the liability of central banks.

The introduction of cryptocurrencies, stablecoins, and many other private initiatives such as Facebook’s Diem presents notable implications for changing the global financial landscape. Therefore, central banks have to strengthen their position with respect to these emerging alternatives to money.

Central banks should review and investigate the possibilities of competitive positioning in a frequently changing financial landscape. Central banks have the primary authority over money, thereby calling for their involvement in propagating a new variant of central bank-backed digital money. This is where you find the foundation for CBDC. Central Bank Digital Currency is basically considered as a new form of central bank money with various concepts surrounding its explanation.

Start your blockchain journey Now with the Blockchains Fundamentals Free Course

What is CBDC Exactly?

The only acceptable definition of CBDC, which provides the basis to understand benefits of CBDC, has been outlined by the IMF. The International Monetary Fund has classified CBDC as a digital representation of sovereign currency issued by a central bank or central monetary authority.

In addition, CBDCs come under the liability of jurisdiction of the central bank or the issuing monetary authority. Another promising approach for understanding the CBDC pros is to take note of their important traits. The important attributes of central bank digital currencies include the following,

- A central bank or a central monetary authority issues CBDCs.

- The central bank or issuing monetary authority backs the CBDCs.

- CBDCs are easily transferrable through peer-to-peer formats.

- CBDCs are practically programmable for any use case.

- CBDCs are considered as the legal tender.

- Central bank digital currency is pegged against a fiat currency.

Curious to know the difference between crypto and CBDC? Here’s a guide to help you understand the differences of Crypto vs CBDC.

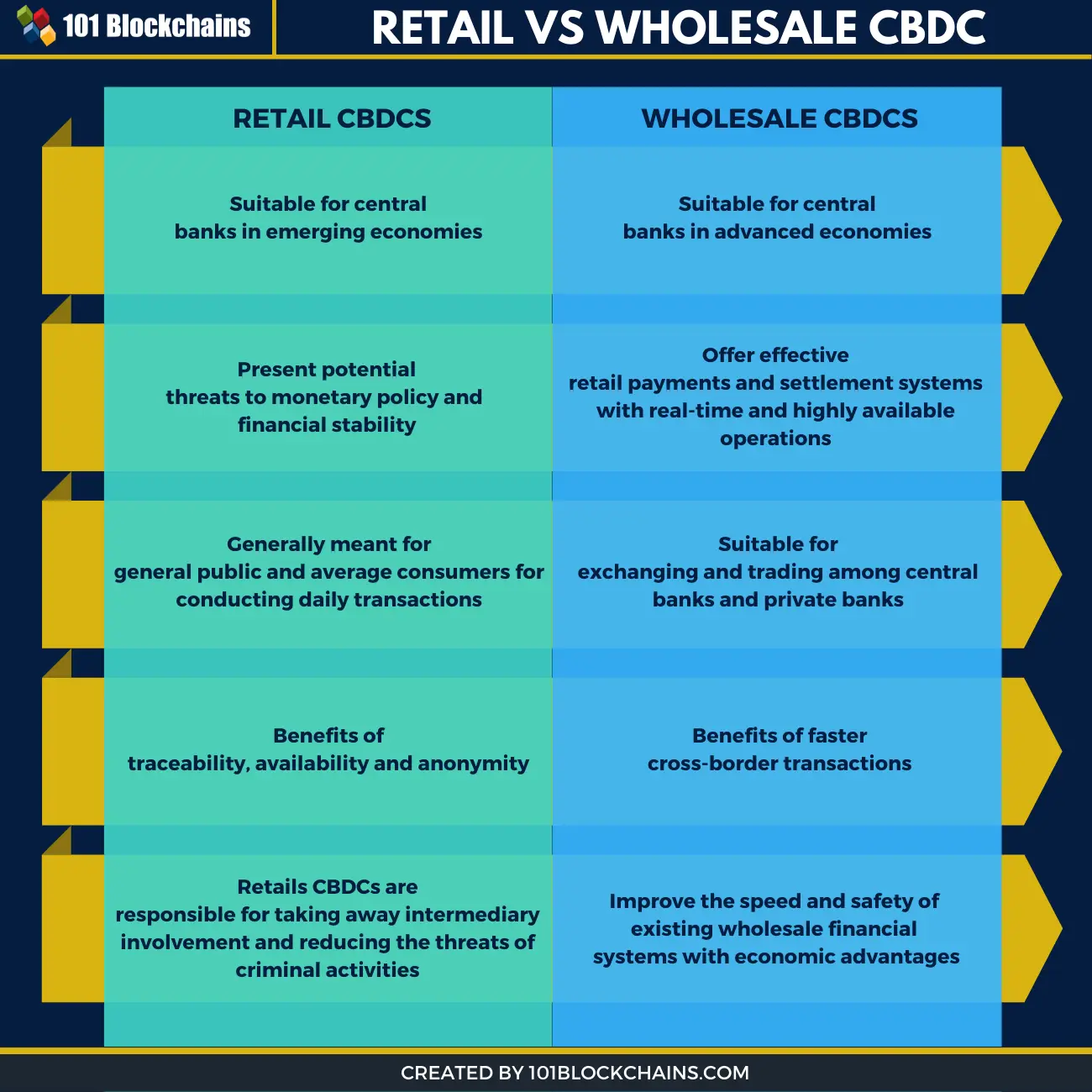

Models of CBDCs

So, CBDC is basically a new electronic form of money that financial institutions, as well as the public, can have in their possession. The choice of adopted model has a profound influence on the functionalities obtained from CBDCs. The advantages of central bank digital currency depend considerably on the functionalities of unique CBDC models. Presently, you can find two notable CBDC models, such as the retail and wholesale CBDC models.

Retail CBDCs are accessible to the public in two different forms, such as digitally issued tokens and deposit accounts in a central bank. Deposit accounts enable businesses and individuals to open an account in their central bank and get benefits from commercial bank services. Digital issued CBDC tokens would offer representation for an electronic alternative to coins and banknotes. Only a central bank could issue these tokens for distribution through commercial banks.

The wholesale CBDC model is also another promising reason for expanding the benefits of CBDC. It can help in ensuring payments and settling transactions among financial institutions. The wholesale CBDC model is not anything new for banks as they could directly access electronic central bank money. On the contrary, the model has the capabilities for improving efficiency and risk management in settlement processes.

Want to know the difference between Retail vs Wholesale CBDC? Here’s a detailed comparison

Advantages of Central Bank Digital Currency

The understanding of CBDCs gives a clear impression of how they are significant for the future of finance. Most important of all, the fundamentals of CBDC provide the appropriate responses for ‘why do we need CBDC?’ effortlessly. It is clear that CBDCs have the potential for transforming the financial industry as we know it. However, it is important to know the specific value advantages they bring to the table.

The pros of CBDCs are an essential requirement for confirming their competitive advantage over other digital currency alternatives. After all, CBDCs are more than just new digital variants of money with the backing of central banks. Here are the notable benefits of central bank digital currency which you would like to consider.

-

Expanding Financial Inclusion

One of the foremost advantages that CBDCs will offer directly rests in expanding the scope of financial inclusion. Even today, a major share of the world’s population is unable to access financial services. Examples of remote areas in developing countries clearly show restrictions on access to bank accounts. Honestly speaking, many banks are not quite eager to reach such regions with their services. In such cases, CBDC pros could ensure easy access to a financial system with low costs and assurance of better efficiency.

The low-cost payment system facilitates transfers between individuals and customers to business through smartphones without holding a bank account. The benefits of CBDC can ensure that people could experience new perspectives on accessing financial services.

Understand the influence of blockchain on the financial supply chain, Through Blockchain In Finance Masterclass

-

Radical Competition to Big Tech Monopoly

The faster adoption of digital money has spurred profound growth in the concentration of power in large tech companies. The large companies serve as reliable payment providers due to the formidable network effect of their platforms. However, CBDCs have enabled the trust of people in blockchain technology in comparison to their nation’s banking system. Central banks could leverage such traits of CBDCs for communicating their abilities to deliver improved resilience of payments system. Therefore, the benefits of central bank digital currency could help central banks in fighting the monopoly of large tech firms.

-

Ensuring Access to Legal Tender if Cash were Unavailable

CBDC could ensure that people could easily access legal tender if cash is not available for certain reasons. In the form of legal tender, CBDC and cash would ha legal recognition as a suitable method for payment. It also represents a claim of liability on the government or the central bank. The advantages of central bank digital currency in ensuring access to legal tender fall in line with declining levels of cash used in payments.

Cash is quite an appealing instrument for money laundering, tax evasion, and other illegal transactions. In addition, it also presents higher security risks in the transport of funds alongside making payments. Governments could also remove cash for reducing crime or improving tax receipts. In such cases, CBDCs would serve as the ideal replacements for cash as legal tender.

Do you want to know how CBDCs is revising the conventional precedents of the financial ecosystem? Check out our guide of Blockchain Solutions For Central Bank Digital Currency to learn more!

-

Better Efficiency in Payment Systems

The next significant advantage associated with central bank digital currencies is the improvement in safety and efficiency of retail as well as large-value payment systems. In the case of retail payments, the benefits of CBDC emphasize improving the efficiency of processes to make payments.

The examples of online, peer-to-peer (P2P), and point of sale (POS) payment systems are some of the instances of payment systems that could be transformed through CBDCs. The benefits of central bank digital currencies in wholesale or large-value payment systems also grab attention. CBDCs could enable faster settlement in large-value payment systems along with longer settlement hours.

CBDCs could also support the exclusion of low-value coins by delivering electronic change. For example, The Bank of Korea introduced a coinless society trial in April 2017. The proposal enabled customers for depositing their change in prepaid cards rather than accepting small modifications from purchase. The considerable saving benefits for the country amounted to almost 36.7 million Euros (the cost of minting coins in 2016).

Get familiar with the terms related to blockchain with Blockchain Basics Flashcards.

-

Faster and Better Cross Border Payments

According to a study carried with the collaboration of the Central Banks of Canada, Singapore, and the UK, CBDC has the potential for improving counterparty credit risk in the case of cross-border payments and settlements between banks. The advantages of wholesale CBDCs are clearly evident in the case of financial institutions and markets. Interestingly, the wholesale CBDC pros could provide the ideal answer for replacing cross-border payments. The advantages of wholesale CBDCs for cross border payments include,

- Wholesale CBDC tailored for a specific jurisdiction that is not eligible for exchange throughout borders presents limited benefits.

- On the contrary, a wholesale CBDC for a specific jurisdiction that is eligible for exchange throughout borders can enhance counterparty credit alongside risks for payment and settlement.

- Another alternative i.e. a single wholesale CBDC accepted universally, could also contribute to improvements in counterparty credit as well as payment and settlement risks.

-

Shift Towards Cashless

The move towards a cashless society is also one of the prominent advantages of central bank digital currency alternatives. Cashless societies envisage the complete exclusion of depending on notes or coins for financial transactions. As people gradually turn towards digital transactions in large numbers and ATM cash withdrawals decline, CBDCs present a favorable alternative. Since it is a digital currency with the backing of a central bank, people are more likely to trust CBDCs.

Start learning Blockchain with World’s first Blockchain Career Paths with quality resources tailored by industry experts Now!

Bottom Line

On a final note, it is evident that the advantages of CBDC can easily pave the way for their future. Central bank digital currencies are a landmark milestone in the evolution of the financial landscape surrounding us. With a competitive advantage over existing digital currency alternatives, CBDCs can offer the assurance of central banks as valuable benefits.

In the long run, the sustainability of CBDC as alternatives to fiat currency and electronic money depends a lot on the ability of central banks to capitalize on their advantages. Learn more about CBDCs and how they can transform the financial services industry altogether with the CBDC Masterclass now!

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!