Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Reviews

Gwyneth Iredale

- on August 11, 2021

Top 10 Blockchain Adoption Challenges

How many challenges does blockchain technology have? Can it overcome all this and shine as a technological blessing? Here, we’ll cover all the blockchain adoption challenges to help you better understand the technology.

The blockchain is still the leading buzzword in the tech world. Protagonists think it will revolutionize the financial sectors including real estate, healthcare, and law. The ability to work in a distributed environment with a tamper-proof facility is the core source behind all these hypes.

However, any new technology will always go through a hype stage. It takes a lot of time to get rid of all the challenges and use it to power the modern world. The blockchain is not different here. Although there are many possibilities, it will still take some time to get over all the challenges.

Therefore, this guide will cover the basics of blockchain problems and their possible solutions to help any novices to understand the technology better.

Top Blockchain Adoption Challenges: What Are They?

Here is the list of the top 10 blockchain adoption challenges that are slowing down the system:

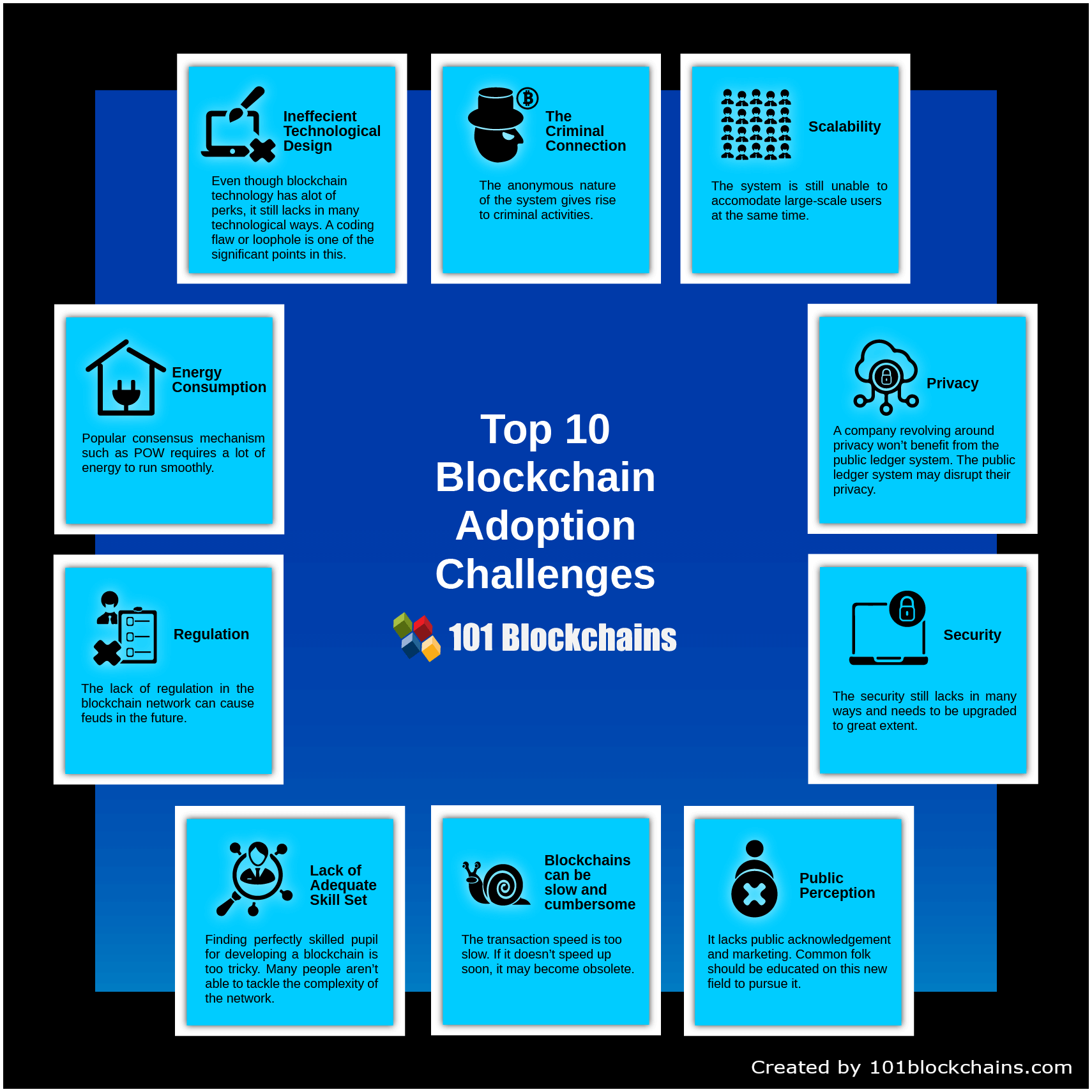

Please include attribution to 101blockchains.com with this graphic. <a href='https://101blockchains.com/blockchain-infographics/'> <img src='https://101blockchains.com/wp-content/uploads/2018/09/Blockchain_Adoption_Challenges.png' alt='Top 10 Blockchain Adoption Challenges='0' /> </a>

Inefficient Technological Design

This is one of the major challenges of implementing blockchain. Although blockchain technology has a lot of perks, it still lacks in many technological ways. A coding flaw or loophole is one of the significant points in this.

Bitcoin was the frontier in this regard, but still, the whole system reeks of inefficient design. Sure, Ethereum tried to cover up all the lackings of Bitcoin, but it’s still not enough.

Let’s take decentralized application development, for example. Ethereum allows developers to implement dApps based on their system. And to this date, there have been many dApps based on them.

However, most of them seem to have a matter of false coding and loopholes. Users can utilize these loopholes and hack into the system quickly. So, all that talk about security isn’t correctly working here.

If we can fix this blockchain adoption challenge, things will surely become more comfortable.

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

The Criminal Connection

The anonymous feature of the blockchain technology attracted not only experts but also criminal personals. Why? Well, the nature of the network is decentralized so that no one can know your true identity.

This makes bitcoin the primary target used as a currency in the black market and the dark web.

Not a good thing to build up the reputation. This bad name is making many people think twice before looking into the whole system. Moreover, it’s natural for people wanting to stay away from any criminal association.

Criminals now use these cryptocurrencies to purchase limited illegal equipment and payment methods. They also ask for cryptocurrencies in exchange as a ransom. The only way to cope up with this is to stop the criminal connection and for all for better blockchain implementation.

Low Scalability

Another one of the challenges of implementing blockchain is scalability. In reality, blockchains work fine for a small number of users. But what happens when a mass integration will take place? Ethereum and Bitcoin now have the highest number of users on the network, and needless to say, they are having a hard time dealing with the situation.

When the user number increase on the network, the transitions take longer to process. As a result, the transactions cost higher than usual, and this also restricts more users on the network.

It can take even days to process the whole transaction. So, in the end, this blockchain adoption challenge is making the technology less and less lucrative.

Few of the blockchain technologies did show us a faster output, but they also slow down when more users log in to the system.

So, this challenge needs to be dealt with pretty fast, as it’s making the whole technology kind of dull.

Curious about the Ethereum Technology ? Enroll now: The Complete Ethereum Technology Course

High Energy Consumption

Energy consumption is another blockchain adoption challenge. Most of the blockchain technology follow bitcoins infrastructure and use Proof of Work as a consensus algorithm.

However, Proof of Work is not as great as it looks. To keep the system live, it will need computational power. You probably heard about mining.

Mining will require you to solve complex equations using your computer. So, your PC will take more and more electricity to overcome this situation when you start mining.

At present, miners are using 0.2% of the total electricity. If it keeps increasing then, miners will take more power than the world can provide. Thus, it now becomes one of the primary challenges of this network.

Many organizations are trying to avoid blockchain altogether just for this challenge. That’s why the situation needs to be under control as it’s one of the main challenges in adopting blockchain technology. But how?

Well, blockchain can utilize other consensus methods to validate the transitions. Consensus algorithms that require very little energy to process.

This is the only way we can genuinely make blockchain technology a blessing again.

Not sure how to build your career in enterprise blockchains? Enroll in How to Build Your Career in Enterprise Blockchains Course Now!

Lack of Privacy

Blockchain and privacy don’t go really well with each other. The public ledger system fuels the system, so full privacy is not the first concern.

But can any organization function without privacy? Well, no. Many companies that work with the privacy needs to have defined boundaries. Their consumers trust them with sensitive information. So, if they are all stored in a public ledger, it won’t actually be private anymore now, would it?

That’s why it is necessary to change the registers to limit access to the data. Making it available for only the customers will be a solution here.

This is an essential requirement in the case of bitcoin and other cryptocurrencies. On the other hand, this raises some concerns for governments and companies. Governments and companies always need to protect and restrict access to their data for various reasons.

This means that blockchain technology won’t be able to work with sensitive information until anyone solves the problem.

Private or federated blockchain can work here. You would get limited access, and all your sensitive information would stay private as it should.

Get familiar with the terms related to blockchain through Blockchain Basis Flashcards

No Regulation

This is one of the main challenges of implementing blockchain in an organization. Many organizations are making blockchain technology a means of transaction. You will see many products depended on this. But even now, there aren’t any specific regulations about it. So, no one follows any specific rules when it comes to the blockchain.

Now, this is where the issue comes in. Although blockchain guarantees visibility as one of its benefits, there is still no security. You won’t know for sure if it will be safe for you or not. To get over these challenges, governments and extremely controlled sectors may need to create regulations for blockchain.

Curious to learn about blockchain implementation and strategies? Enroll Now in Blockchain Technology – Implementation And Strategy Course!

Security Problems

Security is another crucial topic here. We all know how every blockchain technology boasts about its security. But like any other technology, blockchain also comes with a few security loops.

The 51% attack on the network is one of the security flaws of the network. In this attack, hackers can take over the network and exploit it in their way. They can even alter the transaction process and restrict other people from creating a block.

To deal with this, the protocol layer needs more security. We already saw some of its security loopholes by now. However, only a handful of scenarios have good protocols that can cope with this. So, no one knows whether they are safe to use for a long time.

Lack of Adequate Skill Sets

In addition to software and hardware, you must also find qualified personnel to manage blockchain technology. As you know, blockchain technology is relatively new and is still evolving. At the moment, few people have the skills to support such technology.

On the other hand, the demand for this qualified staff is enormous. So, if you want to hire skilled people, you’ll have to pay up large salaries. The right people will cost you.

Like any technological innovation, the blockchain will continue to evolve. Yes, there may be challenges, but they are not obstacles. Adopting new regulations and standards is a must. Before you know it, you are also considering using blockchain technology for your company. So, beware of the blockchain adoption challenges.

Blockchains Can Be Slow

The blockchain is complex. That’s why it takes more time to process any transactions. Also, the encryption of the system makes it even slower. Although they claim to be faster than traditional payment methods, still, in some cases, they can’t deliver it.

Completing a transaction can take up to several hours. So, if you want to pay for a cup of coffee, it will cause you trouble. It’s most suited for making large transactions where time isn’t a vital element. It’s an element of risk. And wasn’t it supposed to remove the ‘unsecured’ nature of blockchains from the equation?

Theoretically, the principle extends to blockchain networks that use something other than store value—for example, logging transactions or interactions in the IoT environment.

These channels – in fact, even computer files – can become slow and impractical. It’s not the case always. It only slows down when the network is staked with too many users. The more it grows, the slower it gets.

This blockchain adoption challenges can become a hurdle soon. So, we should hope for a solution fast. However, some new technologies offer a faster speed compared to the traditional ones.

The establishment has a direct interest in the failure of the blockchain. To be honest – It can disappear faster than we anticipate. So, it’s urgent to find a solution for these blockchain adoption challenges.

Banks earn huge profits through intermediaries. And because of this, the costs are much less than usual. But if blockchain can outrun this factor, it will be much cheaper than this. We believe organizations would have to consider these challenges in adopting blockchain technology.

Banks use tremendous lobbying power with governments and legislators. It is conceivable that, if they decide that it is in their interest, the traditional financial sector can reduce the blockchain. They can also significantly reduce its usefulness and limit its availability.

Sharpen your blockchain skills and become a blockchain expert with 101 Blockchains Blockchain Expert Career Path.

Public Perception

Another one of the huge challenges to adopting blockchain technology is the lack of knowledgebase. In reality, the majority of the public is still not aware of the existence and potential use of this technology. If we want blockchain to be successful, it has to earn acceptance. Even though the technology is making history, still it’s not enough to attract more consumers.

Also, the lack of proper marketing for this niche is making it unpopular. So, if you are not involved with this, you won’t even know it exists.

Currently, blockchain technology is almost the same meaning as Bitcoin. Most people only think bitcoin is the only blockchain network. Others don’t even know about it except the cryptocurrency.

Meanwhile, the value of Bitcoin continues to rise to unprecedented levels. And also, cryptocurrency remains associated with the dark transactions of money laundering, black trade, and other illegal activities.

Before the general adoption is possible, members of the public must understand the difference between bitcoins, other cryptocurrencies, and blockchain. This will help to eliminate the negative implications of cryptocurrencies and make the technology shine by itself. It will be the result in an increased willingness to use the technology.

Want to know more about enterprise blockchain platforms? Check out the best enterprise blockchain frameworks now to understand how each of them works.

Is There Anything More to Blockchain Adoption Challenges?

Blockchain will face different blockchain adoption challenges before it is integrated into society. These include scalability, the time needed to verify transactions, the cost of transactions, and security.

Particular attention has recently been focused on hacking incidents in Bitcoin-based companies and startups. What you don’t know here is that most of these situations are a result of rogue users.

For example, a software wallet, which is essentially the Bitcoin equivalent of a bank account. You have to install this wallet on your PC to access and store all your credits. However, the loophole here is that it doesn’t have any encryption.

So, anyone can access your PC and then take your credits.

Another scenario could be the 51% attack. Users can make changes to the network as they wish if more than 51% of users’ control the power. However, it’s an almost impossible outcome and won’t benefit the attackers tremendously. Moreover, regulations are not yet clear for settlement protocols with cryptocurrency protocols. Blockchain adoption challenges pose a threat here too.

On the positive side, regulators are taking more and more steps in some countries to deal with this situation.

There are no restrictions on how financial institutions can use the blockchain to create and manage their internal networks. This will affect the external use of Blockchain technology, such as payments and transfers.

Central agencies of the United States and the United Kingdom indicate that they want to use a pragmatic approach. This news from the big banks is strengthening this practical approach.

Want to learn more about Blockchain Technology? Check out our blockchain definition guide to learn more about it.

Blockchain Challenges and Opportunities: Is There No Hope?

Even though it may seem like there are only problems with blockchain, there are already a lot of counter platforms in place. For example, Hyperledger offers a multitude of projects focused solely on enterprise companies. Not only that, Ethereum is even working on permissioned platforms that can solve the majority of the problems with blockchain for enterprises.

More so, permissioned blockchain can offer benefits for many industries. In reality, there is already a lot of application and projects live that is working perfectly. So, as you can see, all the problems with blockchain will come with solutions and opportunities.

More so, many companies are eager to implement or use this tech, and they are investing a good amount of money in it. Thus, it’s only a matter of time when we’ll see a big change in society and the economy.

Blockchain can still –

- Disrupt our current financing system

- Transform interbank payments

- Ensure peer-to-peer payments

- Provide opportunities to replace existing mechanisms for exchange.

- Preserve financial information, customer records, and agreements.

Want to learn the basic and advanced concepts of Blockchain and Hyperledger Fabric? Enroll Now: Getting Started with Hyperledger Fabric

Conclusion

However, there are still many blockchain adoption challenges to see a real change in the way financial services use this technology. It seems inevitable that companies should follow it closely and be ready to adjust their services and get the results.

Although there is little doubt that blockchain technology will play a crucial role in both the public and private sectors, this future is even further away than many people think. The list of blockchain adoption challenges mentioned above clearly underlines the need for technological improvements.

In blockchain technology’s current state, the main focus has to be making this new, innovative technology widely available.