Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Reviews

Gwyneth Iredale

- on February 02, 2021

Ultimate Guide to Pros and Cons of Blockchain

In this guide, we will discover the pros and cons of blockchain technology and how you can overcome all the shortcomings of blockchain.

Many blockchain enthusiasts on the market are glorifying blockchain technology to be the next best digital revolution. To be frank, they aren’t all wrong. In reality, technology does change legacy systems, gets rid of middlemen, and introduces a new world to us. However, many do fail to properly weigh the pros and cons of blockchain before they jump in.

With every technology, there will always come advantages and disadvantages; blockchain is on that list as well. So, when enterprises try to figure out blockchain’s full potential, they often forget about the issues.

As a result, many tend to make mistakes and loses resources, and waste time. So, to help you weigh the pros and cons of blockchain, we’ll be covering them in this guide. So, let’s see what the blockchain pros and cons are! But before we jump into the blockchain technology pros and cons section, let’s take a quick recap of what blockchain technology really is.

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

What Is Blockchain Technology?

Well, let’s start with the basics – Blockchain technology is a decentralized ledger system that promotes distributed nature, data integrity, and transparency.

It wasn’t that complicated, was it? Let me explain it in a simpler way. Basically, it’s a ledger system where there are blocks, and every single block is connected in a chain-like structure. So, all the blocks will be connected to the new block and the block.

Furthermore, every single block will contain information, and the chain-like structure would represent the linking process. Anyhow, all the information within the block is cryptographically secured. Other than these, it will also have a hash ID, timestamps, and transactional data.

In reality, in this type of architecture, you’ll end up with a chain of blocks, and this is where the blockchain name came from in the first place. Many of you might confuse it with the database, but blockchain and database are very different in reality.

The best pros of blockchain are that it offers a peer-to-peer connection, so there won’t be any centralized server monitoring your every move.

How Popular Is It Among the Enterprises?

At present, many enterprises are highly interested in blockchain technology. After analyzing the pros and cons of blockchain, many already started their blockchain implementation. According to a recent survey, more than 36% of enterprises are willing to invest $5 million or more in the blockchain.

The 2020 survey was conducted on 1488 global enterprises, where every company was asked how much they are planning to invest. You can check out the percentage form below. However, you should know the survey does not include every enterprise in the world working on the tech.

Thus, the “true” percentage will always vary. If you want to get more information, you can check out the Deloitte survey.

| Investment | Percentage of Enterprises Planning to Invest |

|---|---|

| ≥ $10 million | 7% |

| $5 million - $10 million | 24% |

| $1 million - $5 million | 30% |

| $500,000 - $1 million | 24% |

| < $500,000 | 12% |

| Not Sure | 2% |

| No Investment | 1% |

So, you see, enterprises are also eager to invest in tech. Anyhow, let’s move on to the next segment of the pros and cons of the blockchain guide.

Start your blockchain journey Now with the Enterprise Blockchains Fundamentals

Pros and Cons of Blockchain Technology

There’s a lot of pros and cons of blockchain technology, but among them, we’ll look into the pros section at first. Check out the pros of blockchain from below.

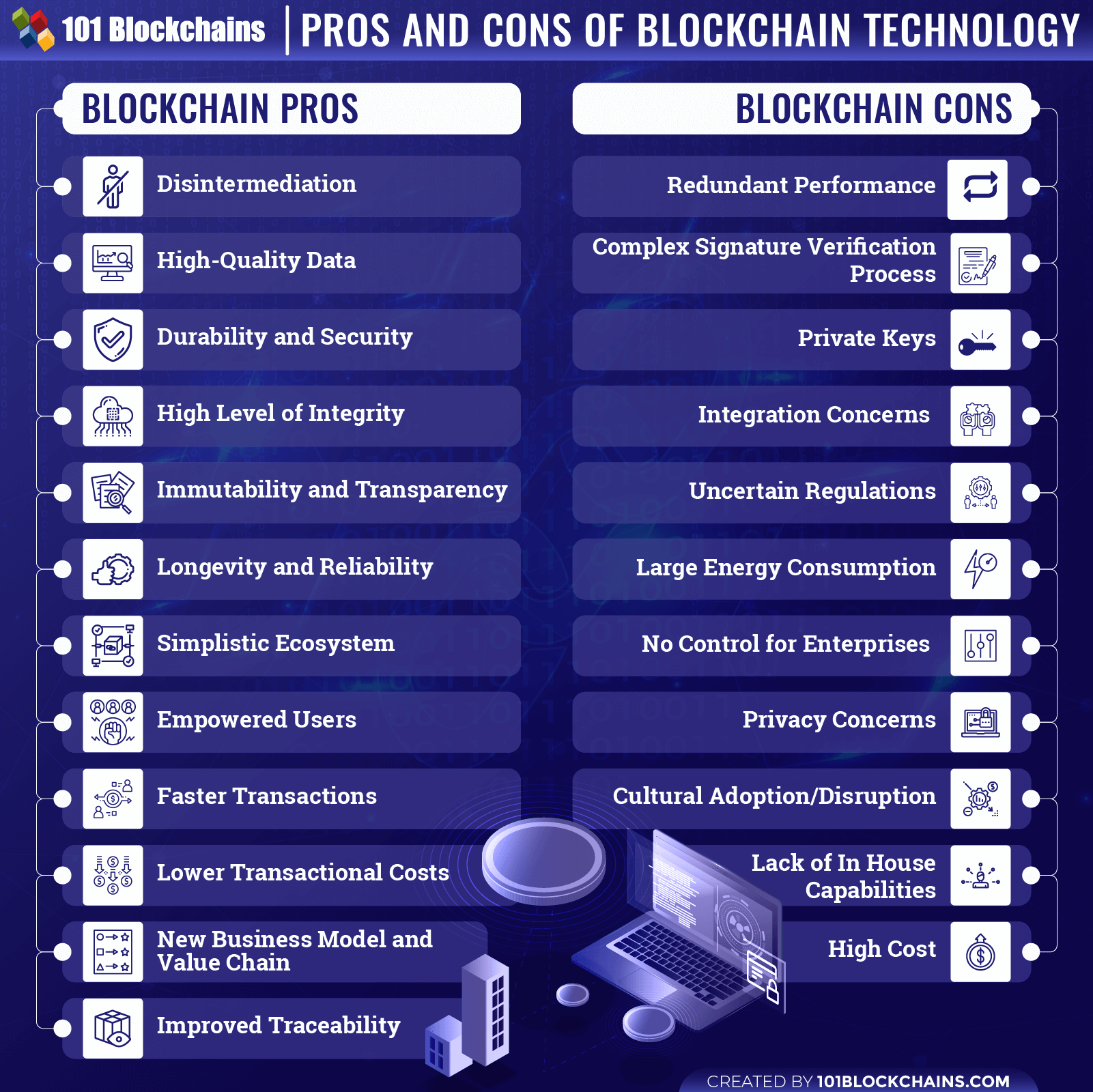

Please include attribution to 101blockchains.com with this graphic. <a href='https://101blockchains.com/blockchain-infographics/'> <img src='https://101blockchains.com/wp-content/uploads/2019/10/Pros-and-Cons-of-Blockchain.png' alt='Pros and Cons of Blockchain='0' /> </a>

Blockchain Pros

There are many benefits of blockchain technology. Let’s see what some of them are:

-

Disintermediation

First of all, with blockchain, you get a distributed system. It means that it gets rid of any middlemen from your system. But how is that an advantage? In reality, middlemen tend to be the third party source that connects you to your services.

However, in the business world, from every service the middlemen offer, they get a cut. In reality, a small amount of payment might not seem like much, but it does add up when your service requires a 10-15 step process.

Other than that, there’s no way of knowing whether the middlemen would be honest with their services. In reality, corruption runs deep, and in many cases, these intermediates tend to abuse enterprises and consumers for their personal gain.

Thus, by getting rid of them, the whole trust issue is solved. Let’s see the next advantage in this pros of blockchain guide.

-

High-Quality Data

Blockchain technology offers a superior level of data quality. In reality, it is a distributed ledger system where it stores data. But how does it provide high-quality data? Well, you need to know that low-quality data would not convert into high-quality data within a night. That’s not how it happens.

Anyhow, this distributed ledger technology offers a consensus process that allows you to filter out any bad data with useful data. It means that no one can just add any kind of information on the ledger or even manipulate the existing ones.

So, when every piece of information is being verified before getting added to the ledger, it will eliminate any false data.

Moreover, it also gets rid of the issues that come from human-made errors. As every single piece of information is verified, there’s no scope for a human-made mistake.

Thus, it significantly increases the quality of data. Anyhow, let’s move on to the next advantage in this blockchain pros and cons guide.

-

Durability and Security

Blockchain offers durability at its best. You could think of it as the internet where there’s built-in robustness. In reality, the overall structure of the technology makes it so durable. Moreover, as it stores blocks of information around the network, it makes sure that there no single point of failure or any single entity controlling it.

This quality makes the system inherently durable. More so, as no one can alter the blocks, it remains to be a solid secured platform. Other than that, it’s quite efficient in fending off hacking attempts as well.

So, there’s little to no possibility of overpowering this network. Anyhow, let’s see the next advantage in this blockchain pros and cons guide.

-

High Level of Integrity

Another great advantage of blockchain is the level of integrity. Compared to any other network systems out there, blockchain offers the highest level of integrity so far. But what does it mean? In reality, it means that all your data will always be the right one, and no one can alter them once it’s on the ledger.

More so, the process of storing the information and consensus processes is also robust. Moreover, any user can’t just make changes to the verification as he/she pleases. Thus, it would offer accurate and reliable data every single time when you transact or store any other information.

On the other hand, every blockchain’s hash ID plays a huge role in maintaining this property. Let’s check out the next advantage in this blockchain pros and cons guide.

-

Immutability and Transparency

For the next advantage in this blockchain pros and cons guide, we’ll be elaborating on transparency and immutability. Blockchain comes with an immutable storage system where you can’t change any single form of data or let alone delete them completely.

In reality, cryptographic hashing plays a huge role in maintaining an immutable structure. As every single block will have a Hash ID, any changes to that block’s data would change the ID drastically. And it’s impossible to recreate the same Hash ID again.

Thus, if anyone tries to change the data, all the other users would notice it right away. Anyhow, most of the ledger system on this technology is also open for everyone to see. Even in private blockchains, there is common ledger information that anyone can see anytime.

-

Longevity and Reliability

Another great advantage in this pros and cons of blockchain guide is the data reliability and longevity. As you already know, blockchain is immutable, transparent, and offer integrity. All of these characteristics result in the reliability and longevity of the technology.

Furthermore, as no one can just change the rules of the blockchain as they please, it remains intact. More so, as it can offer viable solutions for various business issues for the long term, it becomes a reliable technology.

Many enterprises are already considering altering their legacy networks with blockchain for the long term.

-

Simplistic Ecosystem

Many of you may find blockchain to be a complicated ecosystem; however, trust is actually a simplistic ecosystem. In reality, every enterprise needs to go through various stages to process or offer their consumers a solution.

What blockchain does here is to shrink down the various stages of processing into a few steps. More so, as technology can offer almost everything online, it’s much easier to maintain.

There are already many blockchain-based solutions on the market where that offer user-friendly interfaces.

-

Empowered Users

It’s another one of the pros in this blockchain advantages and disadvantages guide. In the traditional centralized system, the users don’t really have that much control over their very own information. As a result, multiple corrupt personnel try to misuse the information for their personal gain.

However, as blockchain ensures a peer-to-peer network and gives users back the control, it ensures no one can misuse them in any way. The level of security and transparency makes sure that every individual is in total control of his/her information.

This is definitely something that we have wanted for a very long time.

Not sure how to build your career in enterprise blockchains? Enroll Now in How to Build Your Career in Enterprise Blockchains Course

-

Faster Transactions

It also offers faster transactions compared to traditional means. Usually, centralized banks can take a lot of time even to process a transaction. It became more eminent when someone tries to send money overseas.

In reality, it could take up to six days to even process that transaction. So, in times of an emergency, many consumers can’t rely on traditional banks’ slow-paced system. However, with blockchain, you can complete a transaction within a few seconds!

That’s awfully faster than any traditional means so far.

-

Lower Transactional Costs

Other than offering faster transactions, it also offers a lower transactional cost—obviously, nothing for free. When you use traditional methods to transact on a daily basis, you have to give them some form of fee in exchange for their services.

Even though the fee might be small, but after a multi-step process, it may become heavier on your pocket. On the other hand, blockchain only offers a lower transaction fee in exchange for a faster transaction process.

Let’s check out the next one in this blockchain advantages and disadvantages guide.

-

New Business Model and Value Chain

Another great benefit of blockchain in this blockchain advantages and disadvantages guide is the new business model. Blockchain comes with a new perspective on how we should model our business in the new world.

With this tech’s use, new marketplaces are being formed, and new opportunities are being created. Furthermore, it’s a better infrastructure that gets rid of a lot of issues we face nowadays. Also, it does add more value to your enterprise once you start to use it by increasing revenues and promoting trust.

-

Improved Traceability

This is the last advantage in the blockchain advantages and disadvantages list so far. Well, it’s more for enterprises that deal with the complex nature of the supply chain or any other similar industry. Tracing back what or how you managed to produce an item is crucial.

In every stage, you need to ensure that it offers the highest quality. However, if you don’t know your goods’ origin, you can’t offer quality. However, blockchain ensures that you can trace these items from the very source to the endpoint.

Not only good, but you can also verify any asset in asset exchanges as well.

Curious to learn about blockchain implementation and strategy for managing your blockchain projects? Enroll Now in Blockchain Technology – Implementation And Strategy Course!

Blockchain Technology Cons

In these advantages and disadvantages of blockchain technology guide, now we’ll talk about the different blockchain technology cons. Let’s see what these are.

-

Redundant Performance

It’s the first con in the advantages and disadvantages of blockchain list so far. In reality, the computation needs of this technology are more repetitive than centralized servers. It’s because every time the ledger is updated, all the nodes need to update their version of the ledger as well.

It’s because the distributed nature of the ledger system mandates that every node should have a copy of the ledger system. Thus, it needs to undergo the same process over and over again.

-

Complex Signature Verification Process

Another con in our advantages and disadvantages of blockchain list is the signature verification process. Basically, for every transaction in the system, you’ll need a private-public cryptographic signature verification.

It then uses the ECDSA (Elliptic Curve Digital Signature Algorithm) to ensure that the transaction happens between the correct nodes. Thus, every node needs to verify the authenticity of the user, which can be a tricky and complex process.

-

Private Keys

To transact on the network, you’ll need to own a private key. Even though other users can see your public key, a private key is much more crucial as it remains hidden. Furthermore, all the blockchain addresses will have a private key.

You need to keep your private key secured by any means if you don’t want other people to misuse your assets. However, if you lose your private key, you’ll lose access to your funds on the network, as well. There’s no way to recover them anymore.

Let’s check out the next con in our blockchain technology pros and cons guide.

-

Lack of In-House Capabilities

As technology is a relatively new concept, there aren’t many capable developers that can work on it. So, when enterprises try to develop their very own enterprise blockchain solution, finding a capable team to handle the project becomes hard.

BAAS providers do offer a lot of services in this case. These services offer high-end developers and marketing teams to help you get your blockchain solution on the market.

Want to know more about BAAS? Enroll Now: Getting Started with AWS Blockchain as a Service (BaaS)

-

Integration Concerns

It’s another one of the major blockchain technology cons. It’s mainly for enterprises that run legacy networks. In reality, blockchain would replace legacy networks. However, the integration process is still not fully functional. More so, many blockchain technologies don’t have the capability to work along with legacy networks.

It means that to use it properly, companies would have to get rid of their legacy networks for good completely. This is something many are skeptical about.

-

Uncertain Regulations

It’s a major con in our pros and cons of blockchain list. In reality, not all blockchain technologies come with the proper set of regulations on the network. Thus, many don’t trust the system at all. On the other hand, the lack of regulation brings in the concept of ICO scams.

And needless to say, many have fallen victim to ICO scams as there is no regulation related to cryptocurrencies. Governmental institutions also struggle to adopt it as this sector runs fully on regulations.

-

Large Energy Consumption

To ensure that every transaction is valid, it needs to go through consensus processes. Obviously, the consensus process requires a huge amount of effort to form every node. Not to mention, all the nodes need to communicate back and forth to ensure that a transaction is valid.

On the other hand, consensus algorithms such as proof of work require a lot of computational power, which increases the overall power consumption. However, you’d be happy to know that now multiple consensus protocols consume much less energy.

Let’s check out the next con in our blockchain technology pros and cons guide.

-

No Control for Enterprises

Well, enterprises need a certain authoritative process in order to use blockchain technology. Unfortunately, public blockchains won’t be able to offer these controlling aspects anytime soon. However, the rise of private and consortium blockchains seems to offer both the technology’s control and distributed nature. These are mostly called enterprise blockchain frameworks, and they are suited for organizations only.

So, we should be able to a more modern approach to this issue much sooner than expected.

Let’s check out the next con in our blockchain technology pros and cons guide.

-

Privacy Concerns

Another major con in our pros and cons of blockchain list is privacy issues. Enterprises need their privacy to maintain their brand value at all costs. Obviously, they can’t reveal their sensitive information to the mass people or their competitors.

And so, many organizations aren’t that keen to use blockchain for enterprise business purposes. However, the use of private transaction options and user-specific authentication is solving this problem bit by bit.

Get familiar with the terms related to blockchain with Blockchain Basics Flashcards.

-

Cultural Adoption/Disruption

This is more of a cultural disadvantage rather than a technical one. Our business models have been running on a specific architecture for quite some time now. But the invention of blockchain threatens that system.

In reality, blockchain already started to change how the system works and has disrupted many industries. As a result, multiple marketplaces have already become obsolete.

Let’s check out the next con in our blockchain technology pros and cons guide.

-

High Cost

Yes, blockchain is much cheaper than other infrastructures. However, it can be a costly solution, as well. Basically, the cost depends on what type of feature you want to add and your needs. More so, developing a solution form of starch requires a hefty amount of money.

Not to mention replacing the legacy system would also cost a lot of money. However, you can overcome this issue if you keep your solutions at a minimum. Moreover, joining a consortium or using a BAAS can help you out as well. However, Blockchain as a Service can help you in developing a solid blockchain business strategy.

According to a recent 2020 survey on 1488 global enterprises, they were asked what their adoption barrier can be. You can check out the percentage form below. However, you should know the survey does not include every enterprise in the world working on the tech. Thus, the “true” percentage will always vary.

| Adoption Issues | Percentage Of Enterprises That Feels The Issue Is A Barrier |

|---|---|

| Replacing or Adapting Existing Legacy Systems | 35% |

| Potential Security Threats | 34% |

| Concerns Over Sensitivity of Competitive Information | 34% |

| Lack of Regulatory Clarity | 32% |

| Lack of In-House Capabilities | 31% |

| Challenges in Forming A Consortium | 31% |

| Burdensome Regulatory Environment | 30% |

| Uncertain ROI | 29% |

| Lack of A Compelling Application | 29% |

| This Technology Is Unproven | 27% |

| Inadequate Funding | 26% |

Additionally, 22% of enterprises aren’t considering this as a business priority. Also, 3% didn’t see any barriers at all, and 1% aren’t sure if there’s a barrier for blockchain adoption or not.

Overcoming the Shortcomings of Blockchain

With every technology, you will have to deal with disadvantages if you want to benefit from the advantages. However, the disadvantages should never overwhelm the advantages. Therefore, blockchain really needs to step up the game.

And that is what it’s doing at the moment. Most of the cons of blockchain applications can become a pro if the companies embrace private or consortium blockchains. Private blockchains offer added control, privacy, regulations, faster transactions, low-cost integrations, and many more.

Also, if you want to get the decentralization of blockchain, you can always use consortium blockchain for your company. As time is going by, more and more people are interested in blockchain technology and masting up the skills they need to build a career in this field.

This eliminates the issue of lack of skilled professionals and creates a new scope for both the employee and the employer. Yes, there is a possibility of new cons to emerge within the blockchain application ecosystem, but don’t forget that there will be pros as well to counter that.

Start learning Blockchain with World’s first Blockchain Career Paths with quality resources tailored by industry experts Now!

Ending Note

Blockchain is a relatively new technology right now with a long journey ahead. So, it’s quite eminent that it will have cons and pros as well. We’ve highlighted almost all the pros and cons of blockchain in this guide.

However, you should note that blockchain has already resolved most of the issues and figuring out a newer way to minimize the issues as much as possible.

So, give it a couple of years more, and you might see a perfect technology ready to disrupt the industries. This is a great opportunity to start learning more about blockchain technology. We recommend our blockchain courses to help you get started on your blockchain journey.

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!