Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Blockchain

Aviv Lichtigstein

- on April 12, 2020

How To Integrate Blockchain In The Telecom Industry

As businesses increasingly turn to blockchain applications to enhance existing services, how can telecom systems benefit from the latest distributed ledger technologies?

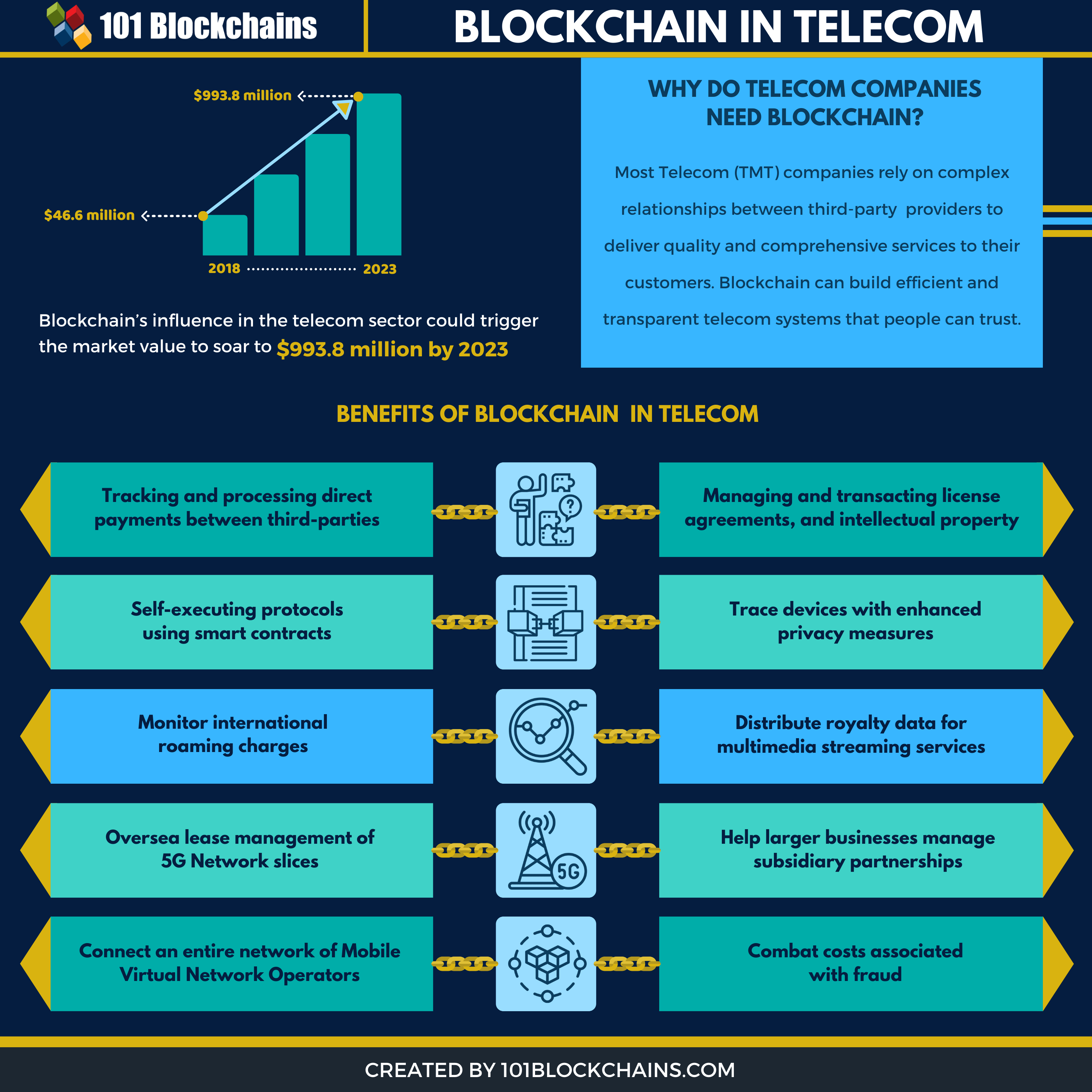

While the telecommunications industry has enjoyed front-row seats to some of history’s most exciting technological developments, blockchain remains a relatively new and untrodden path for today’s telecom businesses. That said, some experts believe blockchain’s growing influence on the telecoms sector could trigger the market value to soar from $46.6 million in 2018 to a mind-blowing $993.8 million by 2023.

Whether you’re a technical director looking for hands-on advice or a CEO wanting to invest in the latest technologies, understanding the value of blockchain will help you open the door to a world of opportunities.

Join us as we explore the potential applications of blockchain in telecommunications and how the industry can overcome long standing barriers to drive innovation and unlock new opportunities for growth.

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

What Is Blockchain?

Before we dive into the nitty-gritty of how your business could benefit from blockchain, it’s essential to understand what blockchain is and why companies might choose to use it.

The term ‘blockchain’ first rose to fame in 2008 to describe a distributed digital ledger of financial records. In the early days, blockchain was used to securely track cryptocurrency transactions by collecting and storing a real-time record of changes on the ledger.

Unlike traditional systems that operate via a centralized database with a single point of authority, blockchain technologies use a distributed ledger that grows with time. Once information enters the blockchain, it’s there to stay. Anyone with authority to access the blockchain can view every change via a continually-updated ledger — synchronized across a dedicated peer-to-peer network.

All blockchains are composed of three core components:

- Block. Any piece of information that enters a blockchain is stored as an individual block. Different blocks are connected via a secure chain to keep a real-time record of how a dataset changes over time.

- Hashing. Every block is secured and tagged by an encrypted digital signature called a hash. To avoid duplicate information, blockchains use a process called proof-of-work to check if each hash is unique.

- Block Time. All blockchains generate new blocks at regular intervals. We describe the frequency of these updates as block time. The shorter the interval, the closer the blockchain is to showing a real-time representation of off-chain events.

Many businesses are interested in how they can use distributed ledgers to build accurate records. Blockchain systems help companies to avoid human error or miscommunication between poorly-connected IT systems. Complex off-chain events can be simplified and recorded into a series of bite-sized chunks.

Why Do Telecom Companies Need Blockchain?

While blockchain technologies have extensive applications in sectors like finance and supply chain management, most telecommunication businesses are yet to feel the full force of this emerging technology.

Most Technology Media and Telecom (TMT) companies rely on complex relationships between third-party providers to deliver quality and comprehensive services to their customers. Blockchain comes into its own when we think about building efficient and transparent systems that people trust.

Some of the core benefits of blockchain for TMT companies include:

- Tracking and processing direct payments between third-parties. Blockchain can help telecom businesses keep on top of transactions, avoid duplicate payments and archive historical data.

- Managing and transacting license agreements, assets and intellectual property. Decentralized digital ledgers can help telecommunication businesses coordinate multiple professional relationships with service providers and B2B customers.

- Reaping the benefits of R&D tax relief. Many businesses who are actively engaged in the development of new blockchain technologies could be eligible for R&D tax credits.

- Self-executing protocols using smart contracts. Businesses can use blockchain technologies to trigger automated invoices, refunds, contract renewals and much more. Smart contracts accelerate outdated processes, avoid errors and minimize reliance on intermediaries.

Please include attribution to 101blockchains.com with this graphic. <a href='https://101blockchains.com/blockchain-infographics/'> <img src='https://101blockchains.com/wp-content/uploads/2020/04/blockchain-in-telecom.png' alt='blockchain in telecom='0' /> </a>

Blockchain Use Cases In The Telecom Sector

Adopting blockchain to enhance efficiency, build trust and improve transparency can help TMT businesses deliver a fast and reliable service that customers love.

Whether it’s handling digital rights in the entertainment sector, processing domain name system (DNS) services in computer science or overseeing chain-of-custody integration in the supply chain, the potential applications of blockchain in telecoms are endless.

Blockchain can also revolutionize the way telecom businesses:

- Trace devices with enhanced privacy measures.

- Monitor international roaming charges.

- Distribute royalty data for multimedia streaming services.

- Oversea lease management of 5G Network slices

For example, Mobile Virtual Network Operators (MVNOs), like Asda Mobile and Virgin Mobile, are subsidiary data carriers that outsource their operations to larger mobile networks, like EE.

Blockchain can help larger businesses manage these subsidiary partnerships and connect an entire network of MVNOs that talk to each other in harmony. So all parties understand what is happening on the blockchain and everyone can keep track of who owes who.

Start your blockchain journey Now with the Enterprise Blockchains Fundamentals

Is Your Company Ready For Blockchain Systems Integration?

While the benefits of implementing blockchain into your business are clear, putting theory into practice is not always so simple. Learn more about benefits of implementing blockchain in the following article.

If you’re new to blockchain and you don’t have the in-house expertise to optimize your existing systems, investing in blockchain technologies can be daunting.

As with any investment, timing plays a crucial role in how businesses decide when, if or how they should approach an opportunity to embrace new technologies.

With the leap to blockchain involving such a fundamental shift in how things are done and requiring a significant rejig of your business’ IT infrastructure, it’s often a good idea to coordinate the transition alongside other digital transformations. This is the best time to introduce a digital-native system to fast-track operations, trace progress and settle agreements.

It’s much easier to integrate a blockchain consortium from the ground-up into a native system than to optimize your existing software. The latter can feel like hammering a square peg into a round hole.

Curious to learn about blockchain implementation and strategy for managing your blockchain projects? Enroll Now in Blockchain Technology – Implementation And Strategy Course!

Conduct a Cost-Benefit Analysis

If you’re a Technical Director or Head of Technology in a telecoms business, one of the biggest anxieties around adopting blockchain technology is cost. As is the case with all innovations, the first rule of thumb is to conduct a simple cost-benefit analysis to gauge whether integrating blockchain will help or hinder your business.

Ask yourself what pain points you’d like to solve and where blockchain can lighten the load.

While the upfront investment might appear expensive, the long-term savings can be significant. Whether it’s using smart contracts to cut out the middleman or automating processes to reduce labor costs, the slow-burning financial savings of blockchain can be huge.

Blockchain brings value to the telecommunications value chain by helping businesses advance their technical infrastructure and move away from outdated technologies. As customers demand enhanced experiences and competitors adopt state-of-the-art systems to drive innovation, telecom businesses must adapt to keep pace with market demand.

Secure and transparent ledger-based technologies provide telecom businesses with dedicated network infrastructures to oversea data-driven services via a single source of truth.

If part of your business model involves licensing or selling Software as a Service (SaaS), blockchain can combat costs associated with fraud, customer relationship management (CRM) and even subscription payments.

A well-managed blockchain system will become the brain of your business. On-chain records help to streamline outdated processes, avoid errors and circumnavigate labor-intensive procedures.

Want to learn all the fundamentals of Blockchain as a Service? Enroll Now – Getting Started with AWS Blockchain as a Service (BaaS)

Four-Step Guide to Successfully Implementing Blockchain

Once you’ve established whether blockchain is right for you, the next step is to think about how and where you can integrate it into your business.

Here’s a four-step guide to help you determine which company processes would benefit from an end-to-end blockchain operating system and how to guarantee a seamless digital transformation:

1. Identify Which Areas Of Your Business Require Blockchain

While the applications of blockchain in the telecom industry are far-reaching, every business is unique. Technical directors should analyze their operations and carefully consider which areas of their company are best suited for blockchain integrations.

Ask yourself the following questions to determine where to channel your resources:

- Do you process rule-based data? Blockchain technologies come into their own when dealing with standardized datasets and predetermined processes that can be recorded in readable blocks. For example, blockchain would be much more useful for tracking 5G data usage than processing customer complaints.

- Can you interpret your data in more than one way? A core benefit of blockchain is the ability to record and store a single source of truth. If you work with ambiguous datasets, you won’t reap the benefits of synchronizing single truths across a peer-to-peer network.

- Do you have any processes that require involvement from multiple stakeholders? The enhanced transparency and accessibility of peer-to-peer networks enable multiple stakeholders to collaborate in harmony. Decentralized digital ledgers ensure all parties are singing from the same hymn sheet.

2. Review Any Legal Frameworks & Compliance Issues

Compliance needs to be at the front of everyone’s mind when implementing blockchain technologies. While most off-the-shelf blockchain operating systems will provide built-in compliance measures, every business must take necessary steps to ensure no stone is left unturned.

Depending on the services you offer, you may need to consider the following:

- Anti-money laundering laws

- Tax obligations associated with domestic and international transactions on the blockchain

- Legal grounding and credibility of smart contracts

- GDPR and industry-specific data protection laws

3. Think About Potential Risks

As with any investment or technological innovation, telecom businesses must consider the risks associated with adopting blockchain.

Whether it’s facing downtime during the change-over period between two systems, struggling to pay-off the upfront cost of implementation, or damaging your reputation through system failures, companies must conduct a comprehensive risk assessment before showing the green light.

While blockchain-implementation requires technical expertise, any conversation about adopting new technologies needs to involve personnel from all areas of your company.

Everyone from cybersecurity consultants, audit committees, finance teams, technical directors and even product teams must play a part in the decision-making process to ensure fair governance and avoid unforeseen problems.

Naturally, some risks may only materialize once you’ve made the transition to blockchain. If this is the case, it’s important to find rapid solutions and adapt before risks become realities.

4. Who Is Responsible For Managing the Blockchain?

While decentralized ledgers are designed to dissolve authoritative control held by a senior group of individuals, all blockchain systems must be managed and overseen by designated personnel.

Whether it’s sourcing technical support in the event of system downtime or tweaking processes to adhere to the latest legal requirements, all blockchains require maintenance of sort.

Think about how you will fund the technical infrastructure, who will offer technical advice and what protocols you need to adapt to different scenarios.

Not sure how to build your career in enterprise blockchains? Enroll Now – How to Build Your Career in Enterprise Blockchains

Outsourcing Your Operations: End-to-end Blockchain Cloud Services

The fastest and easiest way to implement blockchain technologies is to work with a third-party blockchain operating system.

Empower your telecom business with a multi-cloud blockchain infrastructure and a blockchain consortium to manage your on-chain integration. Instead of building your blockchain systems from the ground-up, end-to-end cloud services offer off-the-shelf services that can be tailored to meet your individual needs.

Enjoy the flexibility of swapping between protocols across different areas of your business and gain deep cost, performance and application insights from purpose-built data analytics programs.

Stay Connected with Blockchain Consortia

While businesses are yet to scratch the surface of how they can apply blockchain technologies in the telecoms sector, now is the time for forward-thinking innovators to bite the bullet and lead the way in distributed digital ledger technology.

The industry’s overwhelming dependence on information management, data security and processing transactions, positions telecommunication as the perfect environment to pioneer the latest blockchain technologies.

On-chain consortia connect a group of organizations who share common goals and can combine forces to fuel growth in their industry. Blockchain hosting platforms work with each member of a consortium to create a mutually-beneficial structure that promotes growth.

If your business is looking to streamline outdated processes, cut costs and enhance customer experiences, end-to-end cloud-based blockchain consortia offer the perfect starting block to leapfrog your telecoms business into the modern age.

Start learning Blockchain with World’s first Blockchain Career Paths with quality resources tailored by industry experts Now!

Hello from Ocyan

Need help implementing blockchain into your telecoms business?

Ocyan works with Tier-1 to Tier-3 organizations within the FinTech, Logistics, Energy, O&G and Telecom industries. We help businesses scale, deploy and manage blockchain applications within an enterprise environment.

Our dedicated Cloud Operating System delivers secure blockchain consortia, optimized back-office support, legacy integrations and sophisticated data pipelines to ensure a smooth transition onto the blockchain.

This post is part of the 101 Blockchains for Startups Initiative and written by Evangelos Pappas,

Evangelos Pappas is the CEO of Ocyan and a technologist with a background in leading strategic corporate ventures around Enterprise software, digital transformation, distributed computing and Blockchain technology.

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!