Learn how blockchain truly works, master key definitions, and uncover what makes smart contracts so "smart." Dive into the fundamentals, gain valuable insights, and start your blockchain journey today!

- Reviews

Diego Geroni

- on December 29, 2020

How to Implement Blockchain To Empower Your Business?

Many of you are wondering how to use blockchain for your own business and reap its benefits. We’ll go through the process of how to implement blockchain technology for businesses and help you understand the concept better.

Blockchain technology was initially created to cater to the digital currency trade. However, the tech-savvy world soon realized there are other ways through which blockchain can be employed.

Blockchain technology makes perfect sense for businesses working in a wide range of industries to implement blockchain. If you are still wondering about blockchain making the right fit for your business needs, here is a great guide that can help you reach an informed decision.

For now, you may be wondering about how to use blockchain for your own business and how to reap its benefits. Such problems are always associated with new technologies, so don’t worry, you are not alone. This is exactly why we are here to guide you through the blockchain implementation process in detail.

Curious to learn about blockchain implementation and strategy for managing your blockchain projects? Enroll Now in Blockchain Technology – Implementation And Strategy Course!

How to Implement Blockchain?

Before businesses implement blockchain technology, it is imperative that they first identify what is its best and most relevant use to cement blockchain as a profitable asset rather than a costly liability.

However, as a business leader, you need to first admit that blockchain is here to stay. You simply can’t ignore it anymore. On top of this fact, it provides practical solutions to many of your daily business functional issues.

The best possible move is to implement blockchain. Let’s get started with it!

Explore Opportunities

Don’t you need the inspiration to begin with? Currently, there are quite a few blockchain implementation examples and uses that can inspire you.

Therefore, it is imperative for any new user to gauge the effectiveness of the current uses and choose the best template for implementation in their own company. You should explore the pilot blockchain use cases which are currently being employed in the market.

Banking

The leading blockchain implementation example is the banking sector.

Owing to the number of security breaches online bank systems face and the fact that one of the most notable aspects of blockchain technology is premium security, blockchain implementation was a perfect alternative to the online banking systems.

That is why certain banks have been almost forced to implement blockchain technology in order to maintain customer confidence. This, in turn, has increased the precision, speed, and safety of transactions and online banking in general. In turn, this also aids banks during auditing.

Simply put, blockchain implementation brings transparency and clarity to financial institutions. This is why most of the banks are in love with blockchain.

Want to learn about the practical implementation of blockchain in the financial sector? Enroll Now: Blockchain in Finance Masterclass

Please include attribution to 101blockchains.com with this graphic. <a href='https://101blockchains.com/blockchain-infographics/'> <img src='https://101blockchains.com/wp-content/uploads/2019/01/How-to-Implement-Blockchain.png' alt='How to Implement Blockchain infographics='0' /> </a>

Insurance

This is a prominent blockchain implementation use case example for your business.

For any insurance firm, transparency of data is imperative. Blockchain technology implementation serves to streamline the exchange of such data and ensures that it remains transparent.

This is performed by smart contracts. It authenticates contract terms and determines whether a certain occurrence/situation falls under the terms of the said smart contract.

This results in the customer getting the claimed amount quickly on merit. Subsequently, records are maintained and updated at breakneck speeds.

Needless to say, blockchain also ensures that the entire process is secure and resistant to illicit hackers. This is why there is a huge growth in blockchain insurance applications in the last year, as well as overall implementation in the life, healthcare, title, and auto insurance sector.

Some of the well-recognized blockchain-based insurance companies include:

- Kasko2Go

- FidentiaX

- Everledger

- Ethersic

You can find many more, as many insurance companies are adopting blockchain technology.

Curious about blockchain’s impact on insurance? Check out our guide on blockchain in insurance right now!

Healthcare

It is important to remember that the healthcare industry requires meticulous record keeping. Furthermore, such patient records can contain sensitive information, and therefore, the security of the same is of paramount importance. So, to implement blockchain in the healthcare supply chain, you have to focus on the pharmaceuticals heavily.

While blockchain technology effectively caters to these requirements, it also provides the opportunity to incorporate online payment methods.

This can also help hospitals and medical service providers link up with health insurance firms in order to expedite insurance payments. There is already a lot of pharmaceutical company that invested money to implement blockchain in the supply chain.

Therefore, the choice to implement blockchain technology will prove to be beneficial to both the implementer and customers.

Curious about blockchain’s impact on healthcare? Check out our guide on blockchain in healthcare right now!

Real Estate

This is another wonderful blockchain implementation use case example. With the onset of digital record keeping in the real estate sector, there exists a significant risk of hackers.

These include the altering record details along with rudimentary errors such as bad record-keeping, inaccurate paperwork, etc.

This can cause an inordinate number of losses to unsuspecting ordinary people.

Fortunately, blockchain implementation serves to remove or at the very least decrease the margin of error. This, in turn, helps both the user’s business’s reputation and the customers as well.

Curious about blockchain’s impact on real estate? Check out our guide on blockchain for real estate right now!

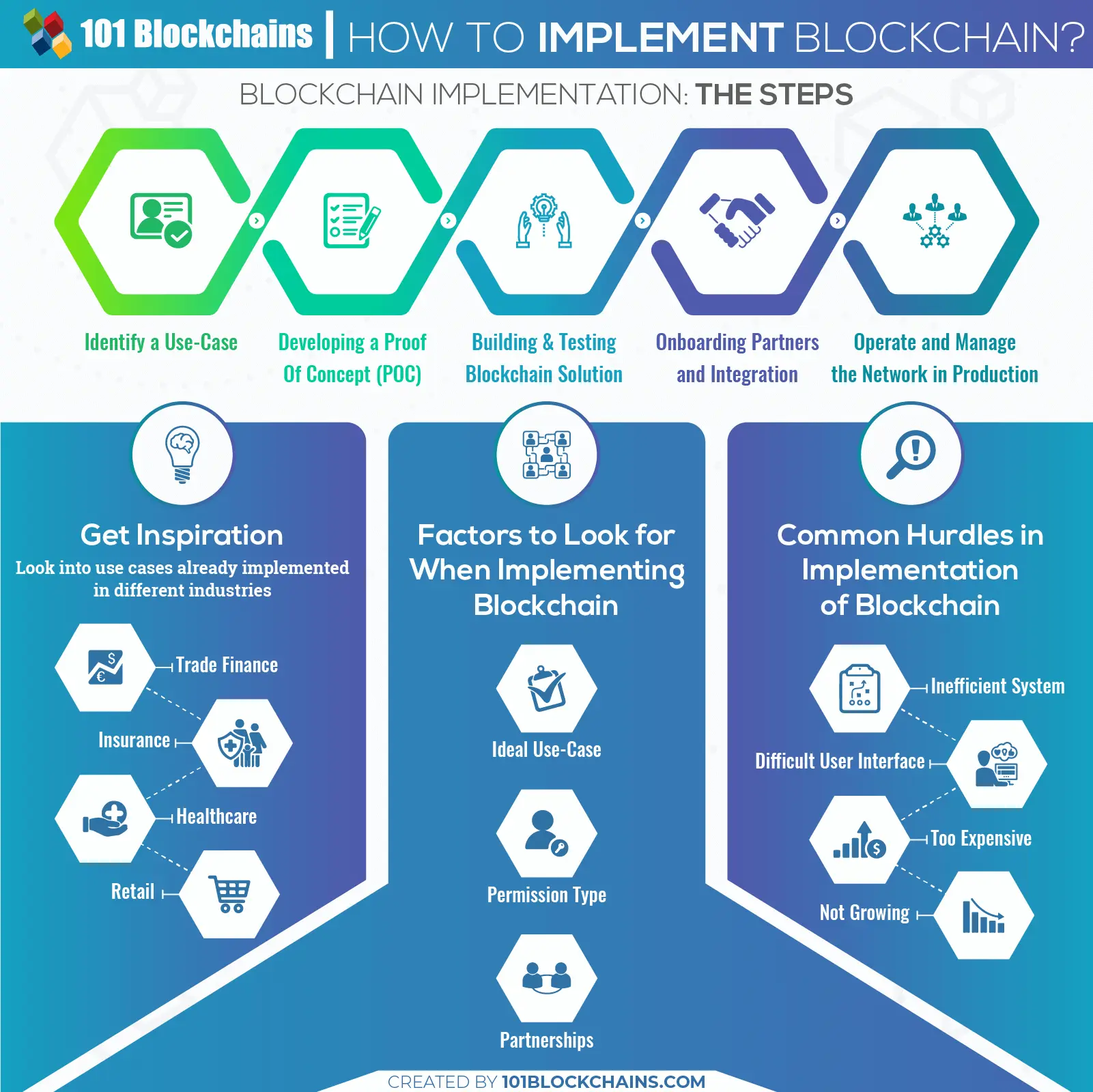

Blockchain Implementation: The Steps

Here are the key steps you need to take for implementing blockchain.

Identify a Use-Case

The first natural step is to identify the use-case. It is a process of identifying, clarifying, and organizing your needs for a blockchain. The use-case answers why do you need a blockchain for your business? For what do you need a blockchain? And what goals are you trying to achieve with blockchain implementation?

It simply adds clarity to your goals related to the blockchain. You identify a use case and then build your next steps around it.

The best thing is to start small. Start with some pilot blockchain use-cases. Explore them, test them, use them, analyze results, and then implement blockchain on a larger scale.

Developing a Proof of Concept (POC)

Once you have overviewed the various ways in which blockchain implementation can benefit your business, you can move on to POC.

Several Fortune 500 entities have already seen the potential in blockchain implementation and are fueling money into developing a proof of concept. In this part, you may have to implement blockchain in java or any suitable programming languages.

-

POC Development Stages

The development of a POC starts like any business venture; with solid planning. The process would start with a series of questions relevant to your project. These questions, in turn, aid the step-by-step development of the POC.

The questions will revolve around the nature of the business and its requirements. It may also include questions regarding the target market, especially if the nature of the market is niche.

After the questions have been answered, you are ready to lay the basic groundwork for your blockchain Proof of Concept. Ideally, you should have a better grasp of your direction. This will avoid any unnecessary complexities during the development of the POC. By extension, preventing complexities will prevent excessive time and money being spent on POC development that lacks direction. This is a crucial stage as you may have to implement blockchain in java. More so, if needed, you may have to go for blockchain implementation in python as well.

Steps to Follow

Here are the steps that you need to follow:

Theoretical Build-up: Set of guidelines that explain the parameter of your project.

Prototype: A prototype that contains code, sketches, architecture, design, and mockups.

MVP: Also called the minimum viable product, with a minimum set of best features.

During the development of the blockchain proof of concept, it is imperative to keep the following advice in mind.

You must identify the result your business wants to achieve or a problem that needs to be resolved via blockchain. Furthermore, do not try to alter the wheel. See if you can use the wheel that is already in rotation.

By that, we mean to say avoid overcomplicating your life by trying to revolutionize blockchain itself and instead, revolutionize your business through blockchain. Testing the sample or prototype is very important. It can mean the difference between millions lost or millions earned.

POC is an important part of implementing blockchain technology. Learn more about it from our ultimate proof of concept guide right now.

Selecting a Blockchain Platform

You should select a platform that suits your budget but also has a concrete history of being effective in your chosen field. Often, one can get mislead by impressive marketing tactics and make the wrong choice. Therefore, research is critical.

While choosing a blockchain platform, you should ascertain whether they possess an open-source station. One should also ensure that their technical team is organized properly.

A good indicator of the platform’s effectiveness is their technical blogs, as most platforms worth your money will have one.

Blockchain as a Service

If you want to implement blockchain in business, then it’s best to go for a blockchain as a service provider. In reality, these providers can help you implement blockchain in your business and manage it. It’s a hassle-free approach to the implementation.

Even though Ethereum is one of the most popular and commonly used blockchain platforms in the world, but for businesses just starting with blockchain, the most effective way to proceed forward is to use blockchain as a service.

This way, you don’t have to invest time in the development of infrastructure, or finding a more skilled human resource, but just kickstart with implementing the pre-designed blockchain that can be customized to your needs.

The best thing is, there are plenty of good options to choose from some of the most recognized tech giants out there. These options include:

- Amazon or AWS (Amazon Web Services)

- Microsoft’s Azure

- Oracle

If you are an SMB, we would recommend you to start with Amazon or their Amazon Web Services (AWS) Templates. This pay-as-you-go service not only allows you to pay according to your use, but the pre-designed blockchain templates make the deployment faster. You also have an option to choose between Ethereum and Hyperledger Fabric as a platform.

Microsoft’s Azure is another cost-effective and quick option for small and medium businesses with plenty of partners as well. However, if you are a large enterprise, we recommend Oracle Blockchain Solution (only available with Hyperledger Fabric).

You can choose between popular options like Ethereum, Hyperledger Fabric, or Hyperledger Sawtooth in terms of platforms.

Want to know the fundamentals of Blockchain as a Service (BaaS)? Enroll Now: Getting Started with AWS Blockchain as a Service (BaaS)

Building & Testing Blockchain Solution

If you are a new user, then you should first observe the current blockchain technologies. Select and implement those that can be modified to suit your needs. For example, you need to look into multiple factors that include:

- Technology depth means security and consensus it offers, and if it supports both public and private blockchains.

- Technology breadth means if it supports multichain and multiple platforms

The key aspect of blockchain technology is smart contracts. This permits people to transfer important products without requiring a central third party. You can attach your required rules to the contracts. Mostly these are blockchain implementation in python.

This will allow the transfer process to be automatic. It also provides transparency and makes sure that all parties follow the rules of the contract. In fact, it is the self-executing smart contract that makes blockchain so exciting for businesses. Create smart contracts for your business processes wherever it makes sense to add automation.

In the case of apps, test them first on the test network to make sure it functions just the way you want it.

Onboarding Partners and Integration

When you want to implement blockchain in your business, you have to consider your partners and stakeholders as well.

You may be tempted to get carried away and switch completely to the blockchain. It is easy to get swept away once you reap the rewards of new technology. You will still need legacy systems and the ability to integrate into the same.

There will be several businesses or firms that will not have incorporated blockchain tech. Therefore, you will be required to liaise with them from time to time. As a result, you will have to integrate legacy systems into your recently implemented blockchain tech. This will allow you to maintain business relations with anyone who has not made the switch yet.

Perhaps you will slowly become a symbol for change. The businesses that have not made the switch will look towards you as an example. In time, they may be convinced that switching to a blockchain is the solution.

They may even come to you and attempt to implement your prototype. In turn, this will open a new avenue of business for you. You may become a blockchain vendor.

But this is only possible if legacy systems are integrated into your blockchain. If they are, it will allow naysayers to appreciate the flexibility of the new technology. If they are not integrated, then the tech might as well be alien to the naysayers.

Start your blockchain journey Now with the Enterprise Blockchains Fundamentals

Operate and Manage the Network in Production

To get things rolling, you can simply build the initial block on your own. However, such a block must incorporate every attribute of the chain.

This process also requires a secondary connection so that the internal correspondence of the blockchain is provided. Think of it this way. In the first step, we laid the groundwork for nodes to send information. Now we shall have to lay the foundation for them to receive information.

This is where an encrypted token or, for the layman, cryptocurrency comes into play. It will be used to harness the computing power necessary to ensure that the communication of the nodes persists.

Deployment

Next is to deploy an application on the blockchain network, which is a prepared application server. It is the step where you host all your applications on the main chain. If you have apps with both on-chain as well as off-chain entities, which makes it a hybrid solution, deploy it on the cloud server.

Want to know more about blockchain technology? Check out our ultimate blockchain definitions guide right now!

Things to Consider When Implementing Blockchain

Here are the quick things to consider and checks during the process of blockchain implementation.

-

Make it Work

If you wish to test whether your system actually works, you have to test it fully. It is essential first to test it in a controlled setting. Then you must also test it in the real work. You may end up finding a unique variable that you did not previously consider. Any factor like that can impact the results of your blockchain implementation.

-

Failure is Always an Opportunity

Every aspect of your blockchain implementation protocol will not function to its maximum at the beginning. Create a copy of all the issues and failures, then try to fix them. You will find many methods to do so. However, you should try to make sure that the blockchain remains simple

Trial and error at such times will be your best friend. Make sure you make enough trials and are not letting any go to waste. Treat each trial as part of your learning curve. Ensure that it allows you to grow instead of regressing.

-

Stay Focused

You must keep your initial target in mind while you are making improvements and edits in your protocol. The different aspects can easily get you mixed up in them.

This can harm your overall plan. Try to see that you and your organization continue to follow what it promised its customers and what they require. Making the system more effective should be your aim, not changing it completely while in the middle.

In short, it is imperative that you maintain focus and not get distracted. Otherwise, the entire exercise could prove to be fruitless for you.

-

Prepare for the Future

Once you are able to create a working blockchain implementation protocol, you should prepare for what comes next. Try and see if some features need improvements. You also need to keep a check if the blockchain is scalable for your future growth needs.

This is important so that the technology does not stagnate. Therefore, you cannot rest on your laurels and must adopt kaizen. Kaizen is the Japanese term for continuous improvement. Continuously work towards perfection in the form of small improvements.

Without a proper business model in mind, it’s difficult to use blockchain as leverage. Check out our ultimate blockchain implementation strategy to learn more about developing blockchain.

Other Aspects to Consider

Here are some other important angles of our Blockchain implementation guide that you should seriously consider.

-

Permission Type

This is an important facet of blockchain implementation and choosing the technology itself. There are 3 types of permission, namely Private, Public, and Federated. You have to decide according to the blockchain presets already available. That is, if the preset is public, but you select a private preset, it may eventually create noticeable hurdles for you.

-

Immutability

Essentially, immutability is what permits a system to notice and check any ‘double-spending.’ At the current stage of its development, the internet cannot cater to ensuring immutability.

Blockchain must have the ability to maintain immutability in transactions. It will keep the relevant information within the network. It will allow individuals to utilize it with appropriate identification. This shall create immutability in the network.

This will provide an additional level of protection, allowing the combined blockchain implementation to have greater localization.

-

Common Hurdles

In establishing your system for the long run, you may face some of the problems, such as those below.

-

Inefficient System

If a new technology is not working to its full, required efficiency, then it does not last long. Bitcoin had similar issues when it began. Customers may not use your blockchain implementation for long if problems in its workings keep rising.

If your blockchain provides them with the same features as other systems but at a greater cost, then customers will not join you. You should always do some market research to see which features are in demand.

-

Difficult User Interface

Some blockchain implementations become too complicated to work with because of all the modifications. All your customers are not very good at using technology. So they will not want to use a system that is too difficult to follow.

Many customers will not have used blockchain technology before. You can appeal to maximum people if you keep your system simple. Your system should not easy rules that most people can understand.

-

Too Expensive

Starting a system from scratch takes a lot of money. With modifications, a project can cost up to millions of dollars. If you are a startup, it will be difficult for you to find such large funds. So you should consider working with other, bigger companies at first.

-

Not Growing

The requirements of customers are increasing all the time. There are many different requirements out there. All these requirements cannot be handled by every blockchain business. Some systems can become outdated soon after they are launched if they do not deal with what customers need.

Start learning Blockchain with World’s first Blockchain Career Paths with quality resources tailored by industry experts Now!

Conclusion

We are sure you now have a clear idea about how to implement blockchain. If you want to implement your own blockchain or simply want to implement blockchain technology into your existing business, this article will help you achieve your goals.

However, it is important to remember that this is still a new technology. You may easily get frustrated at first. The key will be to persevere as this is truly the future of technology and digitalization.

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!