Step into the future of finance—become a Certified Digital Asset Compliance Expert (CDACE)™ and lead with confidence in crypto compliance, auditing, and governance.

- Guides

Diego Geroni

- on February 28, 2021

How to Audit the Next Generation of Digital Assets?

Digital assets are taking over the global economy with new crypto assets and CBDC. Let’s check out the implications of auditing digital assets.

New technological advancements are definitely appreciated across all sectors for the new functionalities they bring to the table. However, the new advancements also bring some concerns that are primarily related to the changes in approaches used conventionally. For example, online shopping allows you to shop for groceries from your favorite e-commerce websites.

However, it also presents some drastic changes in the way you would interact with a product while purchasing it or a business altogether. The same concern has been raised for auditing digital assets, especially with the introduction of cryptocurrency alternatives such as, Central Bank Digital Currencies. So, what should auditors do when they come across new digital assets? Therefore, it is important to find out the best practices in digital audit for the next generation of digital assets.

The following discussion helps you reflect on the responsibilities of management and auditors in auditing new digital assets. Furthermore, the discussion also reflects on the role of regulators in defining the standards for auditing digital assets. In addition, the discussion would also focus on the ways in which audit mechanisms can change with the arrival of new digital assets. Most important of all, the discussion would also reflect on an ideal approach for digital audit with new assets.

Excited to know how the public and private sector work together to improve the financial system? Enroll Now in Central Bank Digital Currency (CBDC) Masterclass!

Problems with Digital Asset Auditing

A few years ago, digital assets seemed like a talk of the future. However, digital assets have taken over the financial landscape all over the world with promising applications across different sectors. You can easily find a new generation of digital assets that are constantly emerging with the assurance of better stability. Some digital assets are also playing on the security factor as their prominent advantages.

For example, Stablecoins have the backing of traditional fiat currencies or a collection of assets and currencies. As a result, they can have the benefits of stabilization in their value alongside ensuring a rise in the number of possible uses of Stablecoins. Therefore, auditing digital assets have become a complicated question for auditors, especially with the gradually increasing prevalence of digital assets in financial statements.

The most notable problem for auditors with newly emerging digital assets is the assumption they should follow about the assets. Should auditors consider digital assets like cash or financial instruments? Therefore, it is crucial for auditors to understand the management’s perspective on digital audits before identifying their own responsibilities.

Want to learn the basic and advanced concepts of Stablecoin? Enroll Now in Stablecoin Fundamentals Masterclass!

Important Points to Consider While Auditing Digital Assets

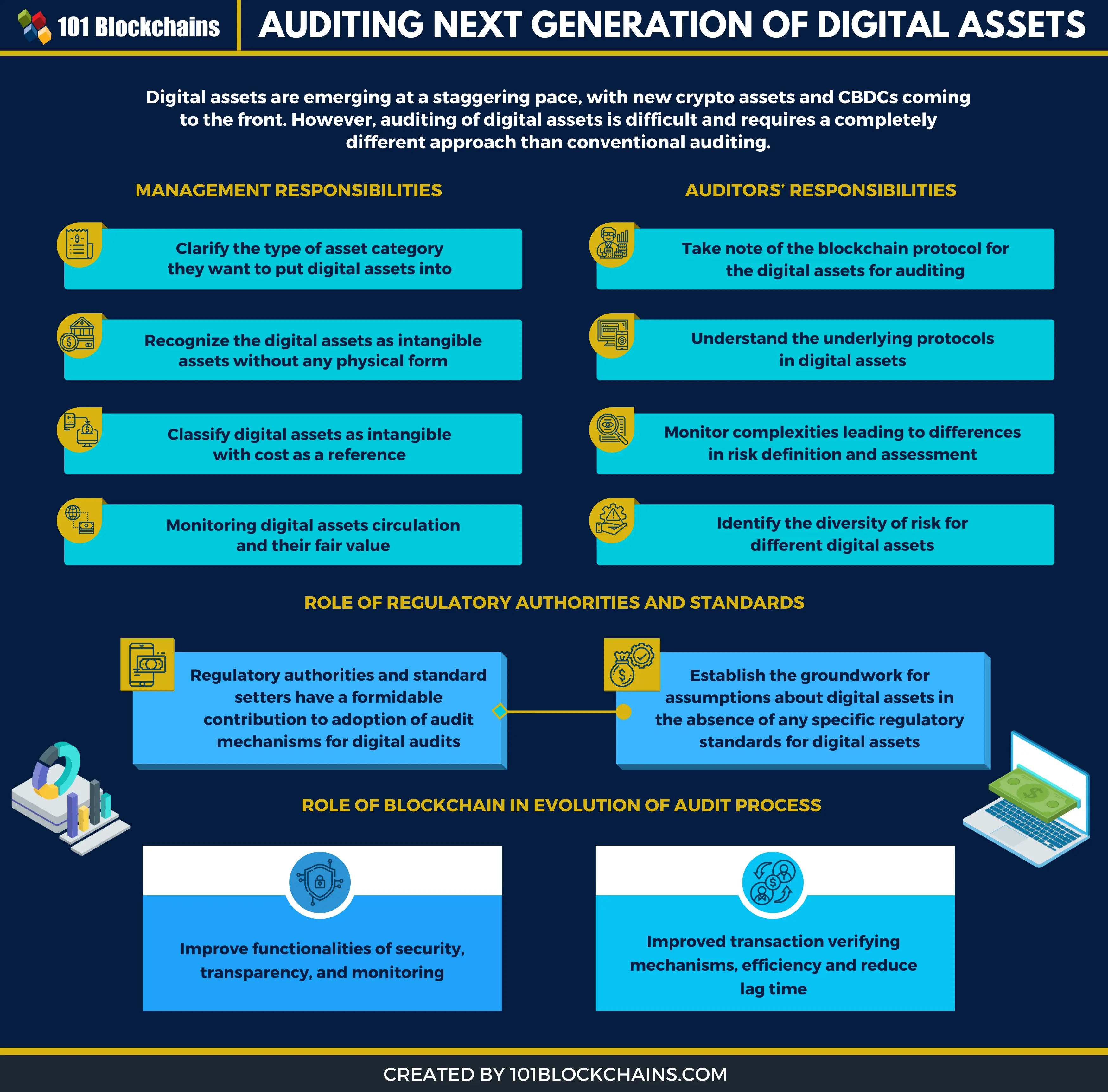

Auditors should understand the responsibilities of management in classifying digital assets and account for them in financial statements. After clarifying the management’s responsibilities, auditors could turn their attention towards methods for offering assurance about their fair presentation. So, let us take a look at the various responsibilities of the management in the processes for auditing digital assets.

Responsibilities of Management

One of the first points in digital audit refers to the diverse terms and conditions associated with digital assets. Therefore, digital assets could also serve distinct purposes even in the same organization. Let us take the example of cryptocurrency as one of the evolving use cases of the digital assets for this discussion, especially with the wide range of uses of cryptocurrency. The most common assumption regarding cryptocurrencies in the existing market suggests them as intangible assets.

The existing market treats cryptocurrencies as assets that are not inventories. Therefore, cryptocurrencies could not comply with the definitions of cash or other financial instruments in certain cases. Now, let us find out the factors that create barriers in considering cryptocurrencies as cash or financial instruments. The following factors can help in building the foundation for understanding the process of auditing digital assets.

According to the International Financial Reporting Standards, cash is supposed to serve as a medium of exchange and monetary unit for the pricing of goods and services. Cash is also the basis of measuring and recognizing all transactions in the financial statements. On the other hand, you could not find any cryptocurrency that aligns with the traits of cash.

The IAS 32 standard, according to International Financial Reporting Standards, also helps in defining financial assets. Generally, a financial asset refers to any type of asset that is either cash or an equity instrument for another entity. The financial asset could also be a contractual right for receiving cash or other financial assets from other entities. It could also be a contractual right for exchanging financial assets or liabilities with other entities according to conditions.

Financial assets could also be specific contracts with possibilities for settlement of equity instruments of the concerned entity. Auditing digital assets such as cryptocurrency present many doubts for auditors as they don’t satisfy the definition of financial assets. Cryptocurrency does not qualify as cash, contract with a counterparty, or an equity instrument of another entity.

A closer overview of these factors points out the remaining intangible assets. The intangible assets could promote possibilities for economic benefit in the long run, and they don’t have any physical presence. However, intangible assets are identifiable and come under the control of the entity. In addition, intangible assets are also excluded from the scope of other standards.

Cryptocurrencies don’t have any physical substance like other new forms of digital assets. Therefore, the digital audit should consider digital assets as intangible with the cost as a reference. On the other hand, a revaluation model is also a reference for digital assets by continuously comparing the amount carried by the digital asset in comparison to its fair value on the measurements in later stages.

Want to become a Cryptocurrency expert? Enroll Now in Cryptocurrency Fundamentals Course

Responsibilities of Auditors

With substantial clarity regarding management responsibilities in auditing digital assets, it is important to find out the auditor’s responsibilities. The diverse approaches for accounting could create many challenges for auditors. Therefore, many efforts are currently under development for achieving consistency in auditing practices all over the world.

Some of the notable authorities in the field of accountancy, such as the American Institute of Certified Public Accountants and the Center for Audit Quality, have taken a proactive stand in achieving a consistent approach to auditing practices. These accountancy authorities have introduced working groups that focus particularly on the management of emerging technologies such as digital assets.

On the other hand, there are many obstacles to auditing processes before ensuring complete alignment of auditing approaches and procedures. However, the promising opportunities in the future would gradually lead to the convergence of all working groups for managing digital audit procedures.

The auditor would have to take the first impression of the actual blockchain protocol implemented. As a matter of fact, this is the first responsibility of an auditor in auditing digital assets. For example, the blockchain assurance team at Ernst & Young works to understand the nature of digital assets. In addition, the team also evaluates the underlying protocols in the digital assets for a comprehensive assessment of evidence from blockchain technology.

Furthermore, auditors should also bear the additional complexities that lead to variations in the definition and assessment of risks according to the concerned digital asset. In addition, the approaches followed by the client for transactions can also be a crucial contributor in terms of complexity. Therefore, auditors could easily find a varying assortment of factors with dominant influence throughout the risk spectrum.

The increasing diversity of risks in auditing digital assets is one of the dominant concerns for auditors. For example, digital assets with better maturity are likely to have more interested parties such as miners, holders, and developers. At the same time, digital assets are also pinned directly with other widely accepted economic claims such as Stablecoins pegged against fiat currency or gold-backed cryptocurrency.

Auditors should note one of the major setbacks in the case of digital assets pinned against widely accepted forms of economic claims. Such type of digital assets could present various risks in comparison to the ones which do not have intrinsic value. The native digital assets such as Bitcoin and utility tokens do not have any intrinsic value and present limited risks.

Auditors should also notice the additional complexity associated with asset-backed tokens in the digital audits. Asset-backed tokens generally bring additional complexity by bringing the smart contract functionality into account. At the same time, auditors should also consider the other factors that determine the position of a specific digital asset on the risk spectrum.

For example, auditors must consider the frequency of the use of concerning blockchain and the number of developers using the blockchain. In addition, auditors must also find out whether the concerned blockchain is open source or not.

Auditors should also take note of another crucial responsibility in auditing digital assets. It is important for all auditors to find out whether transactions are started off manually, or they go through automatic execution through a smart contract. In the case of automatic execution of transactions, auditors have to take note of many other concerns. First of all, auditors would encounter risks of incorrect or unauthorized transactions due to various factors.

Auditors should consider software flaws or hack like some of the factors that could affect manually executed transactions. In addition, the digital audit should also consider the implications of possibly inaccurate information from third-party data feed services or ‘oracles.’ Automatic transactions with digital assets depending on such inaccurate information could are vulnerable to risks. Above everything else, auditors face considerable difficulties in verifying the existence of digital assets in comparison to conventional assets.

Build your identity as a certified blockchain expert with 101 Blockchains’ Blockchain Certifications designed to provide enhanced career prospects.

Role of Regulatory Authorities and Standards

The role of governments in establishing regulatory precedents is undoubtedly significant for various enterprise operations. Many governments know that introducing new regulations for monitoring and auditing digital assets can improve the protection for businesses and investors. On the other hand, it is also reasonable to consider the lack of consistency in regulations throughout different jurisdictions.

The two most contradictory approaches in regulations for monitoring digital assets in Luxembourg and India showcase how regulatory differences can influence digital audit processes. Luxembourg introduced the first nationwide licensed Bitcoin exchange and presented a viable platform for encouraging the use of digital assets. On the other hand, an inter-ministerial committee in India is planning proposals for the criminalization of transactions in private cryptocurrencies.

At the same time, auditors should also note that the International Accounting Standards Board has not classified digital assets in its standard-setting activities presently. On the other hand, the International Accounting Standards Board continues to monitor digital asset development in collaboration with other standard-setting authorities. In addition, the IASB and standard setters also monitor the significance of digital assets for International Financial Reporting Standards.

Therefore, auditing digital assets in existing situations requires adaptability to be existing and emerging situations, methodologies, tools, and context. The new digital assets and the pace of their arrival point out the need for active engagement in developing new tools and methodologies. Most important of all, auditors must also focus on enhancing systemic and effective examination for achieving the desired outcomes.

Want to become a bitcoin expert? Enroll Now in Getting Started with Bitcoin Technology Course

Role of Blockchain in Evolution of Audit Process

The process of digital audit might appear very complicated at present, especially with the different concerns regarding digital assets. First of all, there is no clear understanding about what type of asset category digital assets fall in. In addition, there are no clear legal precedents regarding the classification of digital assets. Therefore, the domain of auditing digital assets can encounter various complexities.

On the other hand, a clear understanding of the role of blockchain in evolving the auditing process can provide a better impression of best practices for auditing digital assets. Blockchain technology can offer reliable prospects for streamlining financial reporting and auditing processes. In the present times, a CPA auditor receives account reconciliations, journal entries, trial balances, supporting spreadsheet files, and sub-ledger extracts. The documents are generally provided in a wide variety of manual and electronic methods.

All the digital audit processes start with varying information requirements and schedules. As a result, a CPA auditor has to invest a considerable amount of time in planning a particular audit. In the case of blockchain-based digital assets, CPA auditors can have almost real-time data access through read-only blockchain nodes. As a result, the auditor could obtain the desired information for audits with better consistency in a recurring manner.

The gradual migration of entities and processes to blockchain solutions creates better prospects for efficiency in accessing information in the blockchain. For instance, recording a particular class of transactions for an industry in a blockchain could help a CPA auditor in developing software solutions for a continuous audit of organizations by using blockchain. As a result, blockchain can help in reducing the burden of manual data extraction and audit preparation services in auditing digital assets.

The faster audit preparation activities could also contribute to a reduction in lag time between transaction and verification. The reduced lag time can create opportunities for improving the effectiveness and efficiency of financial auditing and reporting. Lower lag time in digital audit helps management and auditors to turn their attention towards transactions with higher risks and complexity.

The support of blockchain-based digitalization could also play a crucial role in defining the best practices for auditing digital assets. Auditors could capitalize on blockchain-enabled digitization for leveraging the benefits of improved automation, machine learning, and analytics capabilities. As a result, auditors could easily find unnatural transactions in real-time without any discrepancies.

Furthermore, blockchain also allows the facility of encryption and secure storage or linking of supporting documents to a blockchain. CPA auditors could also access the audit evidence as a trustworthy element for improving the speed of digital audit processes. It is also important to note that the audit process for digital assets will be a continuous process.

However, auditors must employ professional judgment in the analysis of accounting estimates and other judgments by the management. Furthermore, it is also important to evaluate and test the internal controls over data integrity of all relevant financial information sources in case of automated aspects in auditing digital assets.

Best Approach for Digital Asset Auditing

So, what is an auditor expected to do with so many radical changes with a digital audit process? The auditor has the responsibility of collecting evidence according to the management’s perception of the fair presentation of financial statements. In addition, auditors must acknowledge the difference in nature of procedures executed and the evidence collected for traditional audits and auditing digital assets.

Auditors must aim at implementing their expertise and work collaboratively with all stakeholders to develop a comprehensive approach in accepting, design and executing audits for digital assets. Auditors have a crucial role in maintaining the confidence and trust of customers in capital markets. As new forms of assets take center stage, auditors must focus on adaptability as the best practice. At the same time, auditors must also focus on systemic examination and reliable analytical thinking alongside developing new tools.

Start learning Blockchain with World’s first Blockchain Skill Paths with quality resources tailored by industry experts Now!

Bottom Line

On a concluding note, it is clearly evident that auditing digital assets are a complicated process. First of all, there are many views regarding the perception of digital assets. The varying designs, functionalities, and objectives of digital assets also create confusion for auditors.

However, the management could establish a clear scope for digital audit processes by specifying their objectives and classifying digital assets with policy-backed definitions. Readers could also know how blockchain-based solutions can present better prospects for efficient digital asset audit mechanisms. If you want to learn more about auditing digital assets, then you can take our CBDC Masterclass right now!

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!